Photo Credit: sanga park / Alamy Stock Photo

Photo Credit: sanga park / Alamy Stock Photo

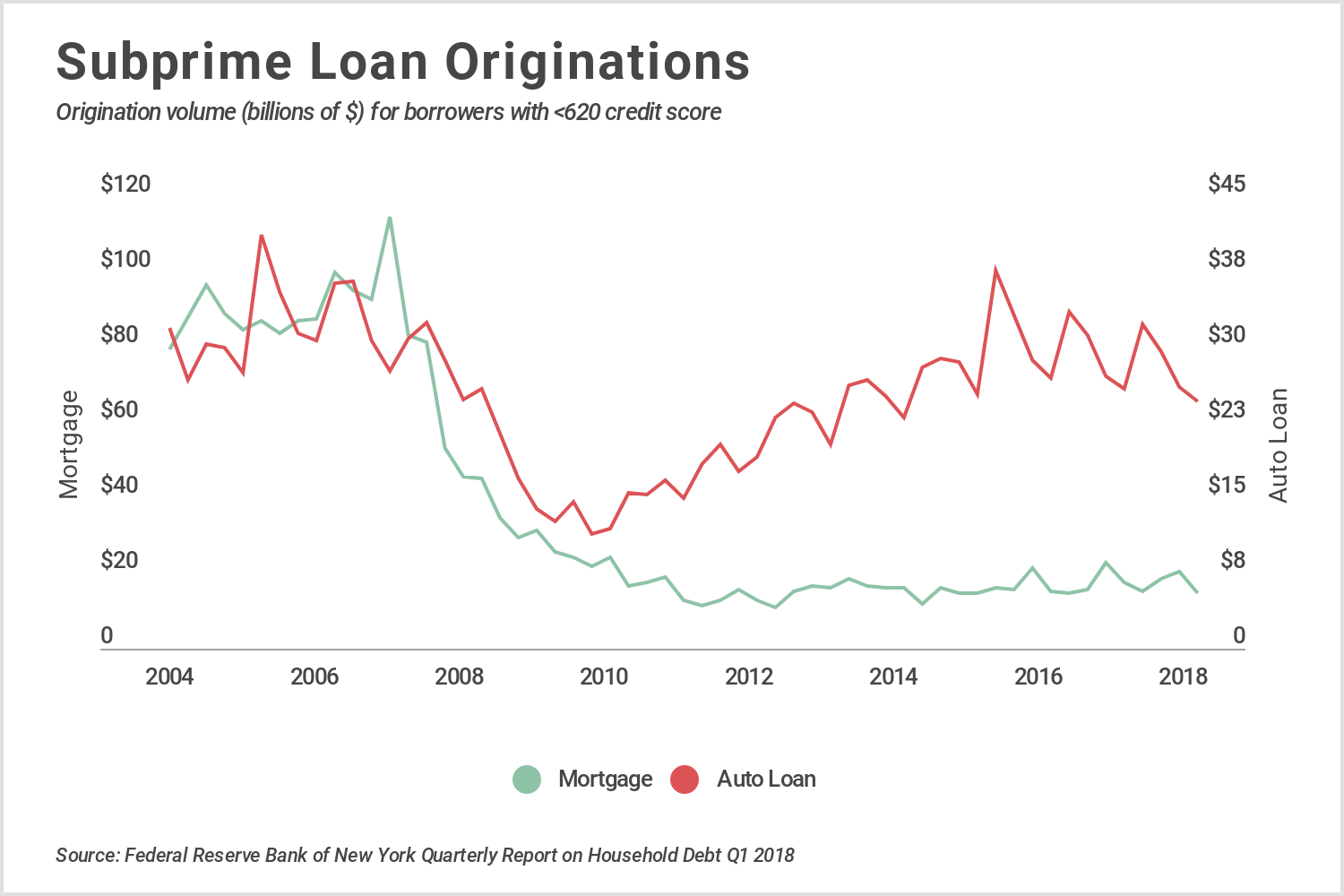

A record number of Americans are taking out car loans. That’s according to the latest New York Fed Quarterly Report on Household Debt and Credit, which shows that since 2012, auto loan balances in the U.S. have skyrocketed, hitting a record high of $1.3 trillion in Q1 2018. Unlike mortgage balances, which have grown slowly since the recession, auto loan balances have increased 67 percent over the last six years, far outpacing the 16 percent increase in total debt over the same time period.

Today, auto loan debt makes up 9.3% of total household debt (up from 6.7% in 2012), and more people have car loans than mortgages—a recent trend that can, in part, be explained by differences in borrowing requirements across the two loan types. While subprime mortgage originations dropped and have remained low since the recession, auto loan originations across the spectrum of credit risk have grown.

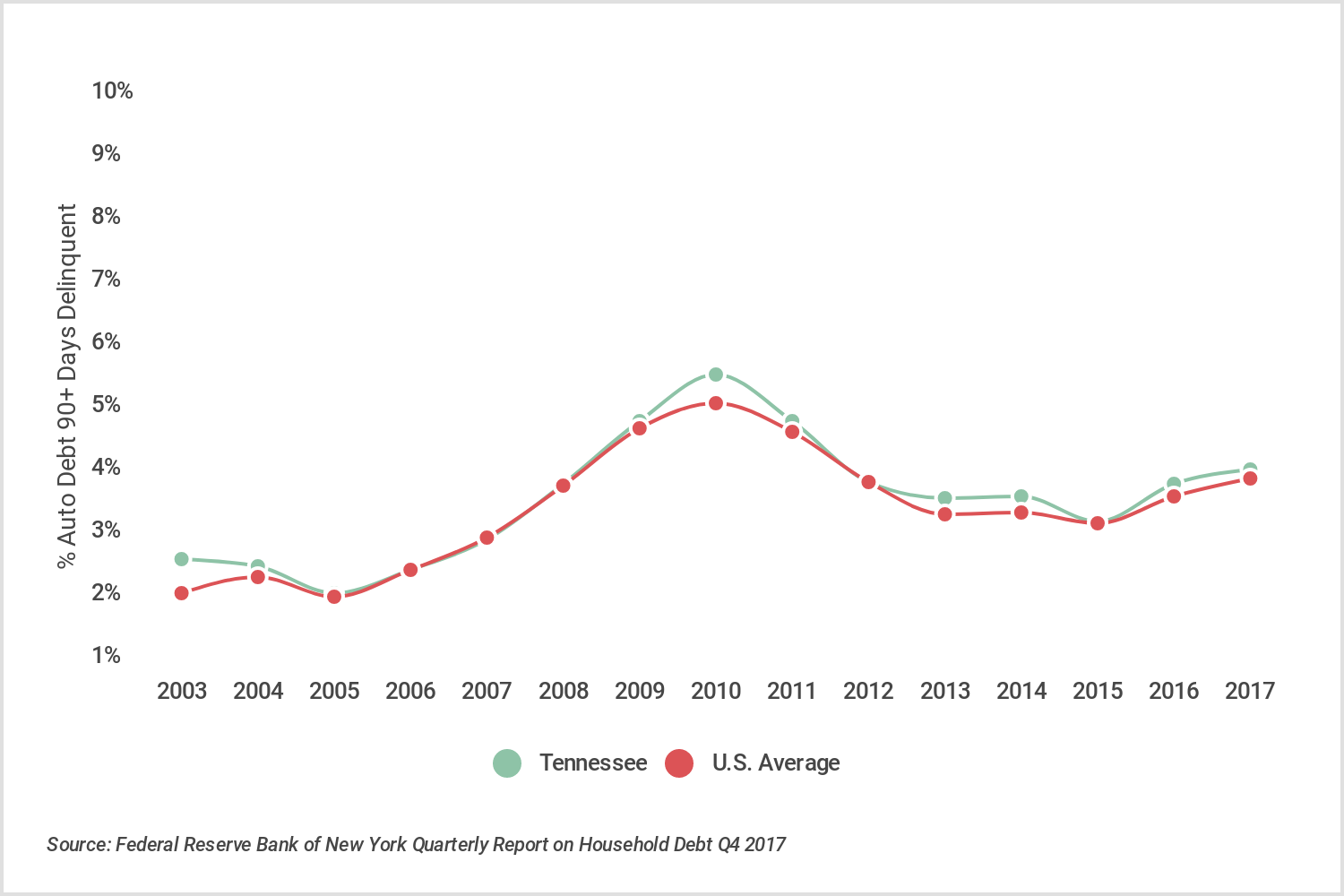

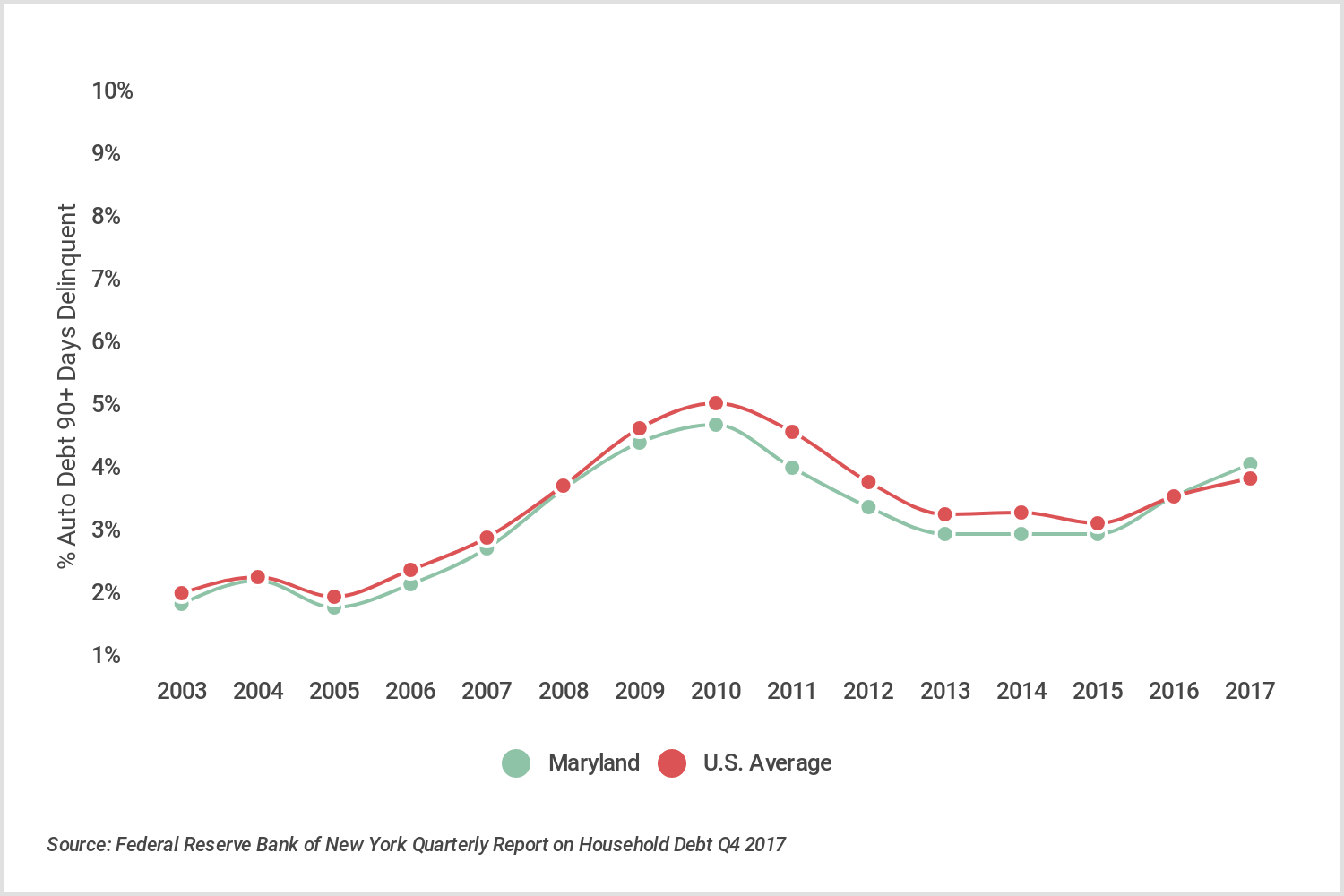

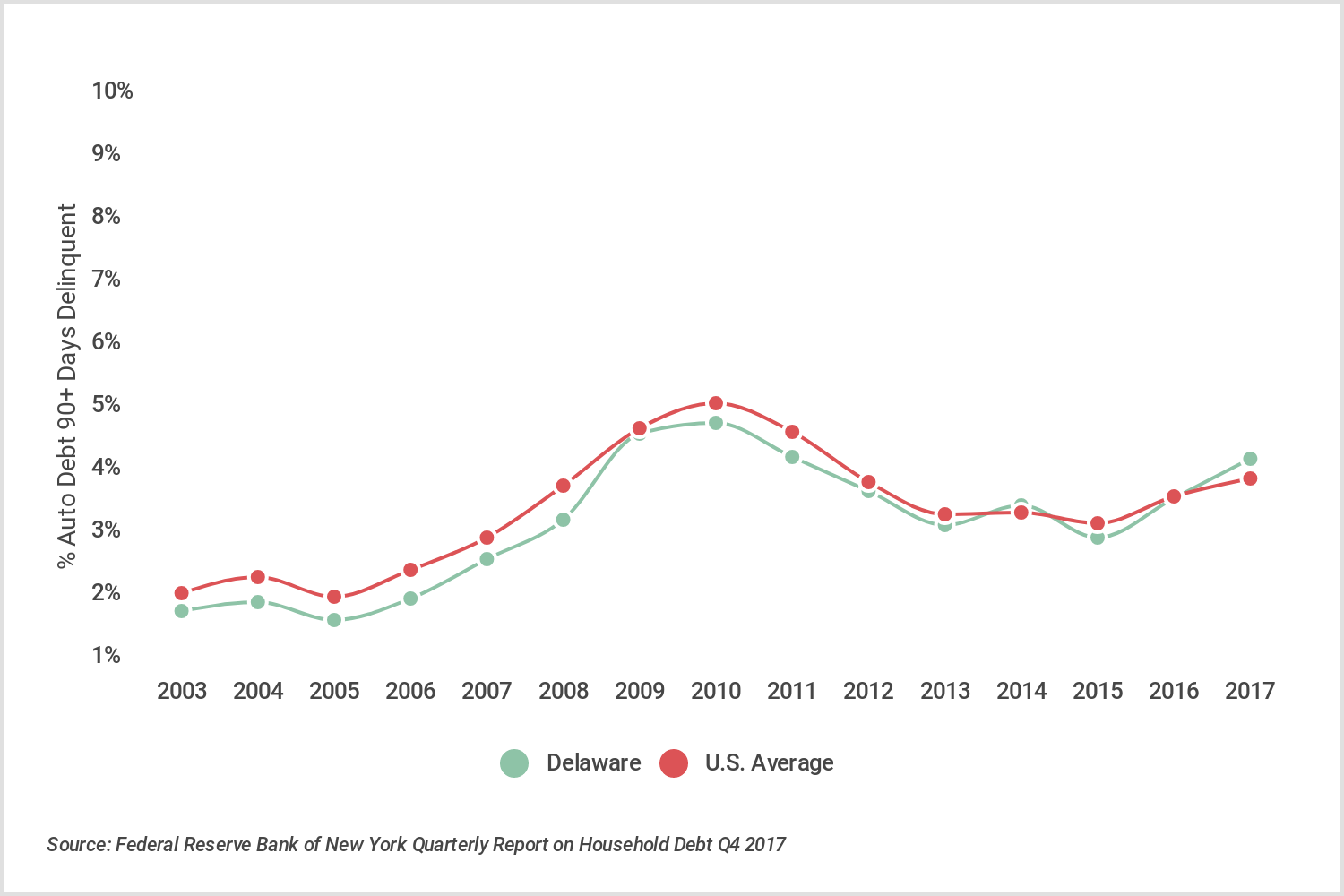

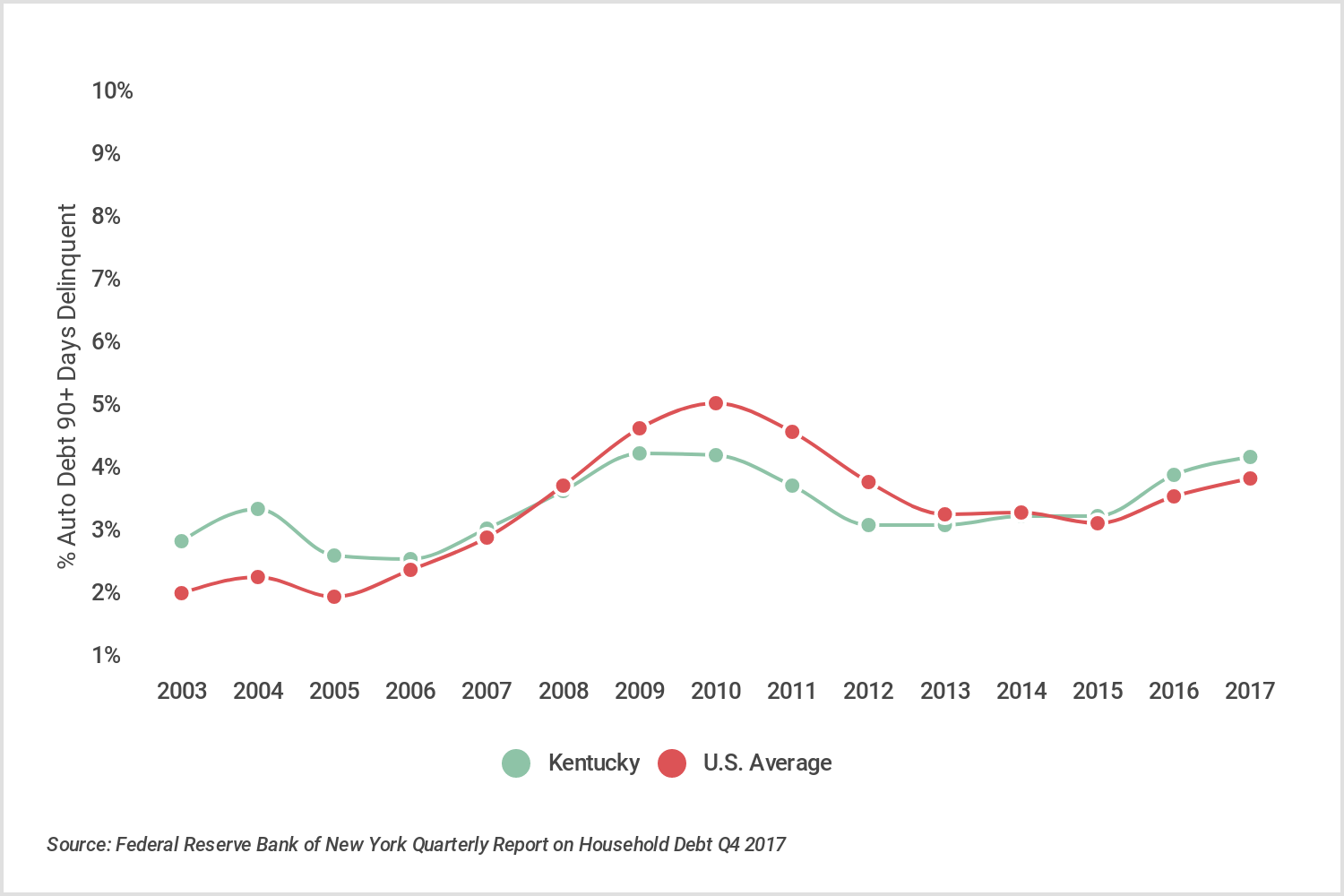

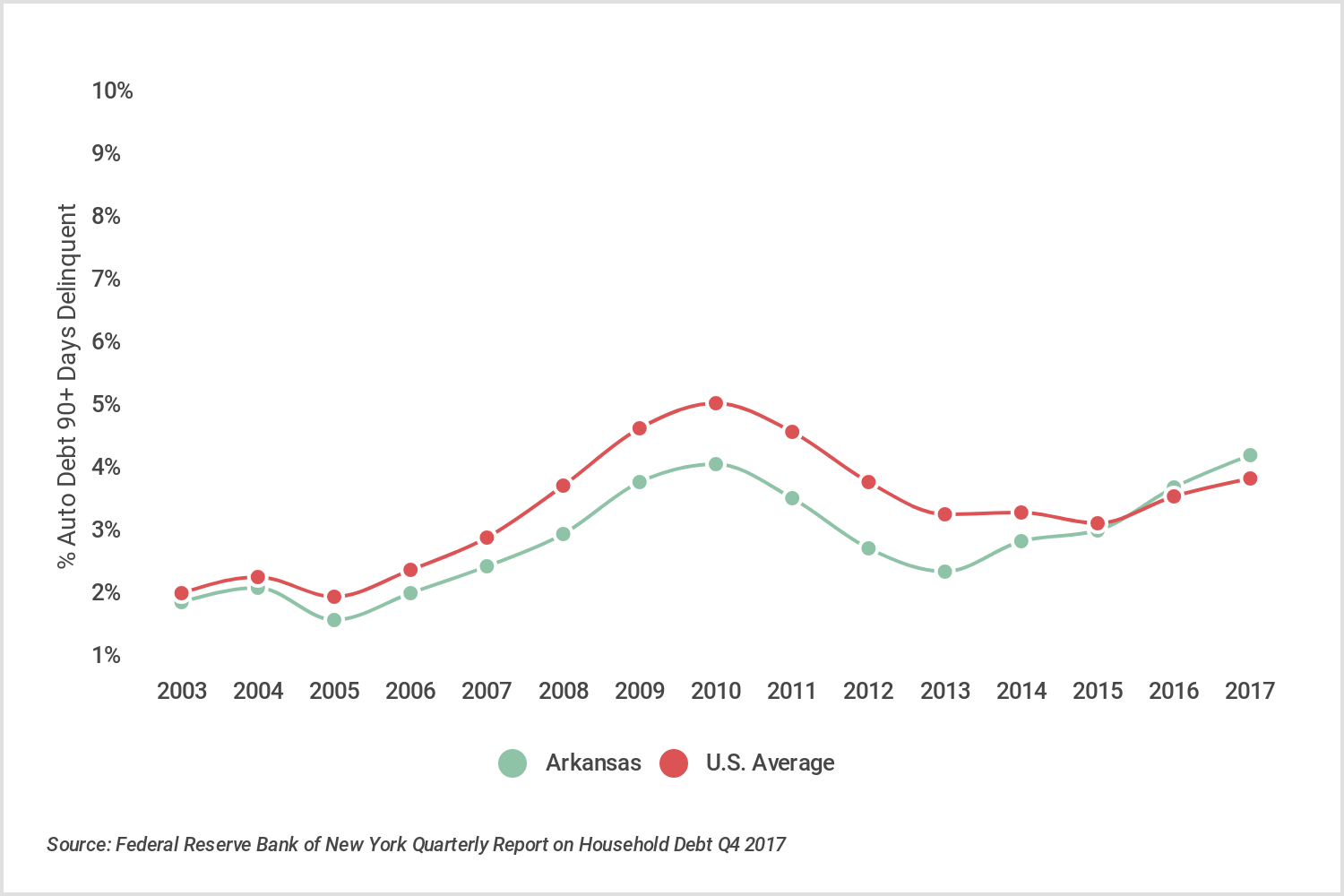

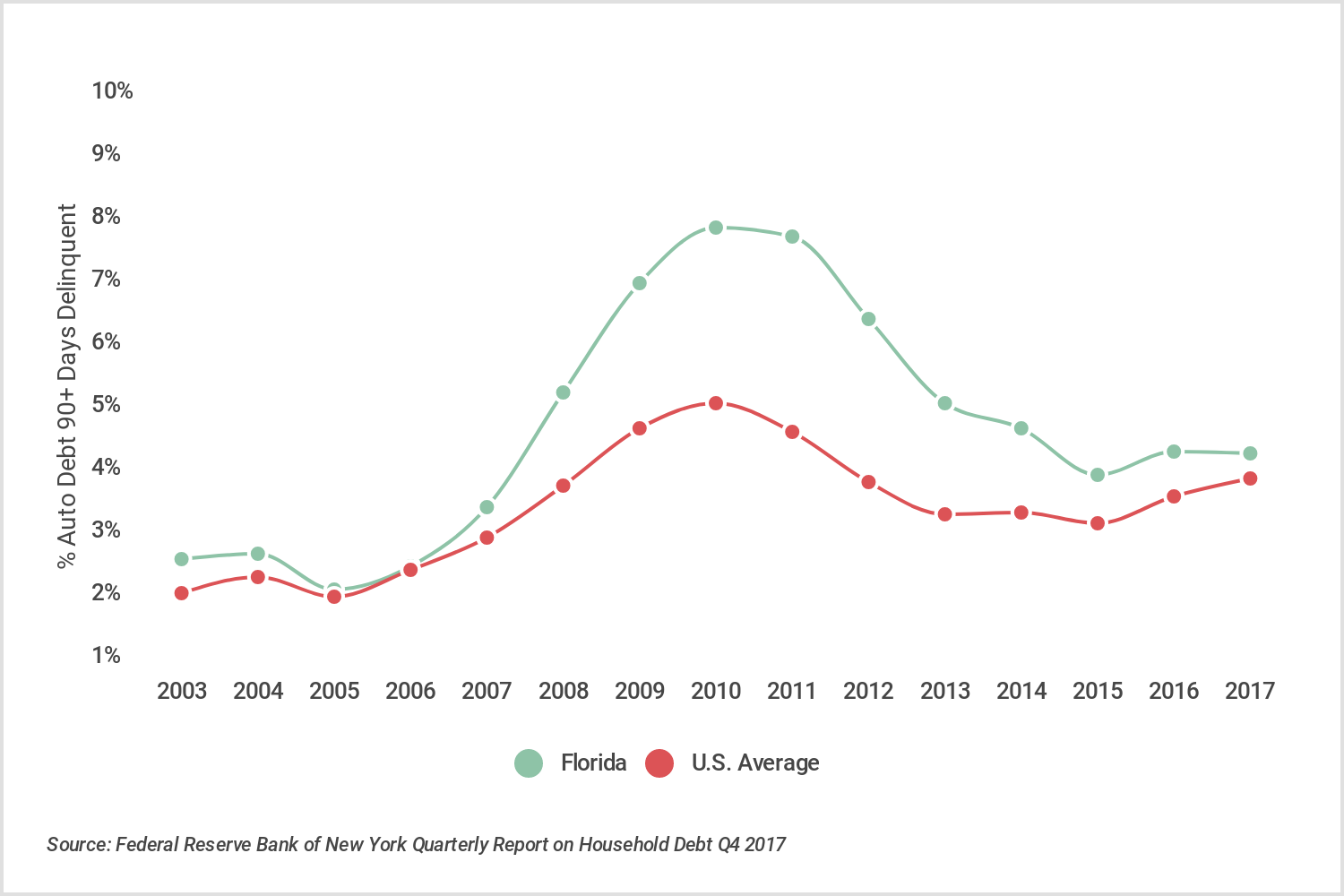

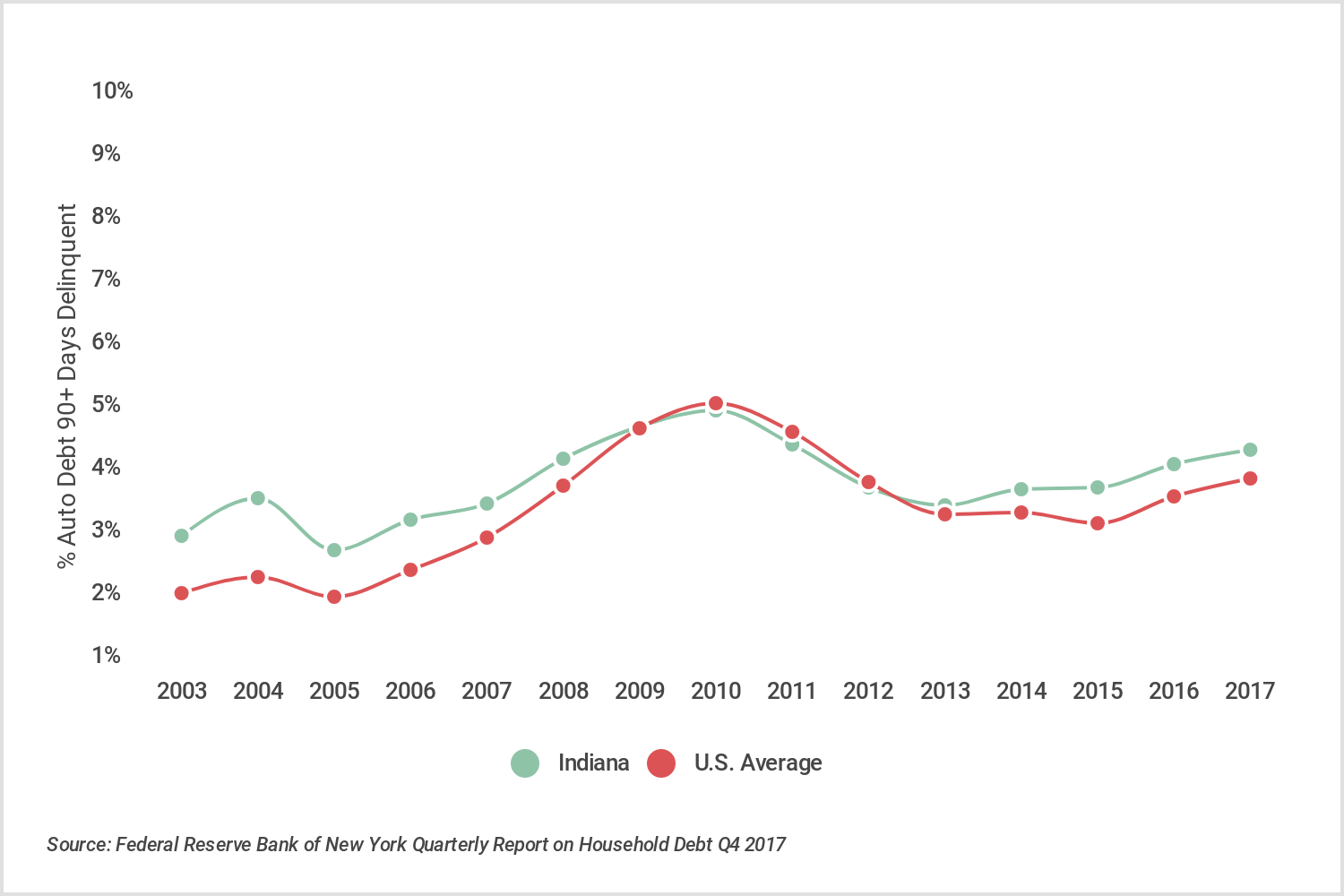

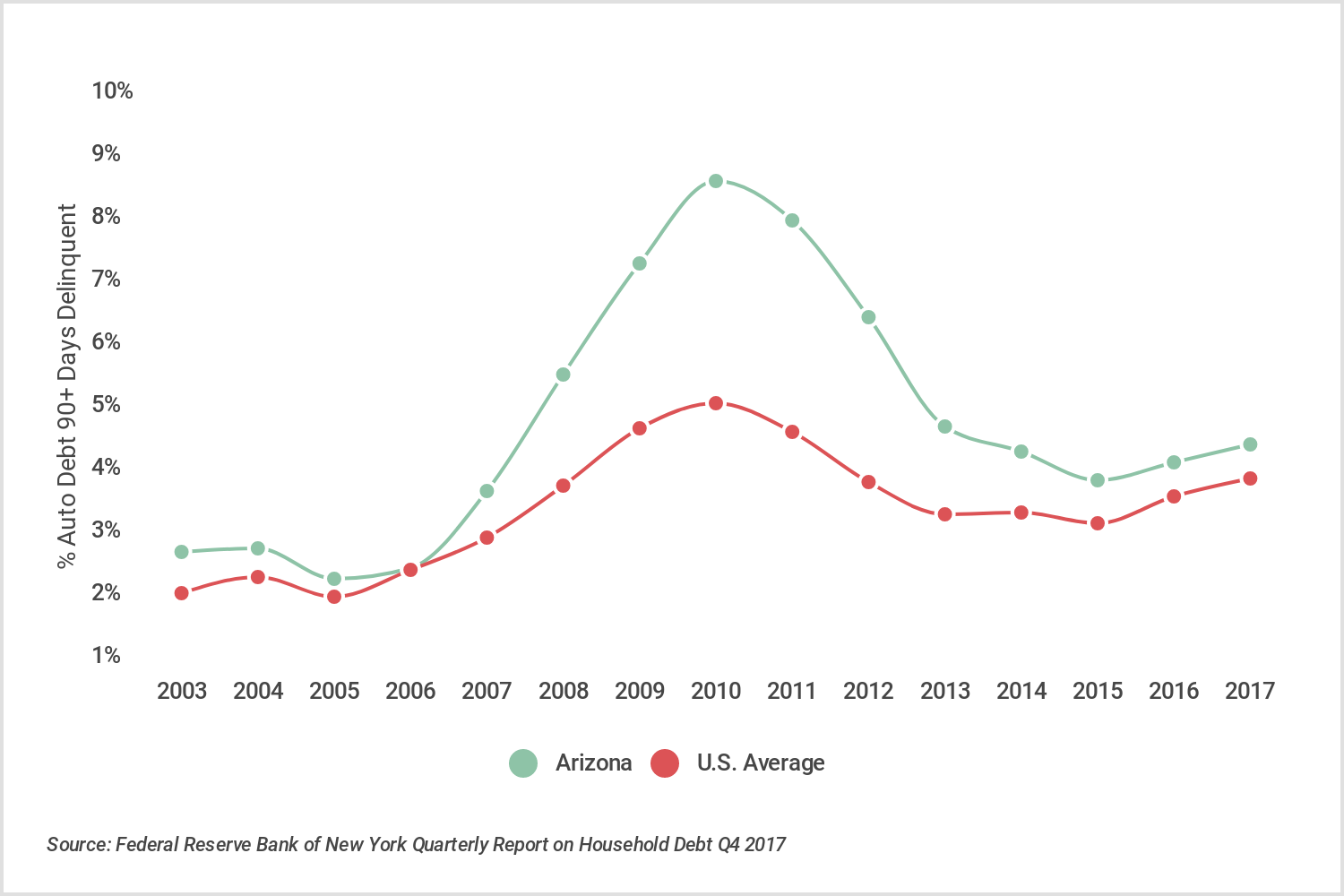

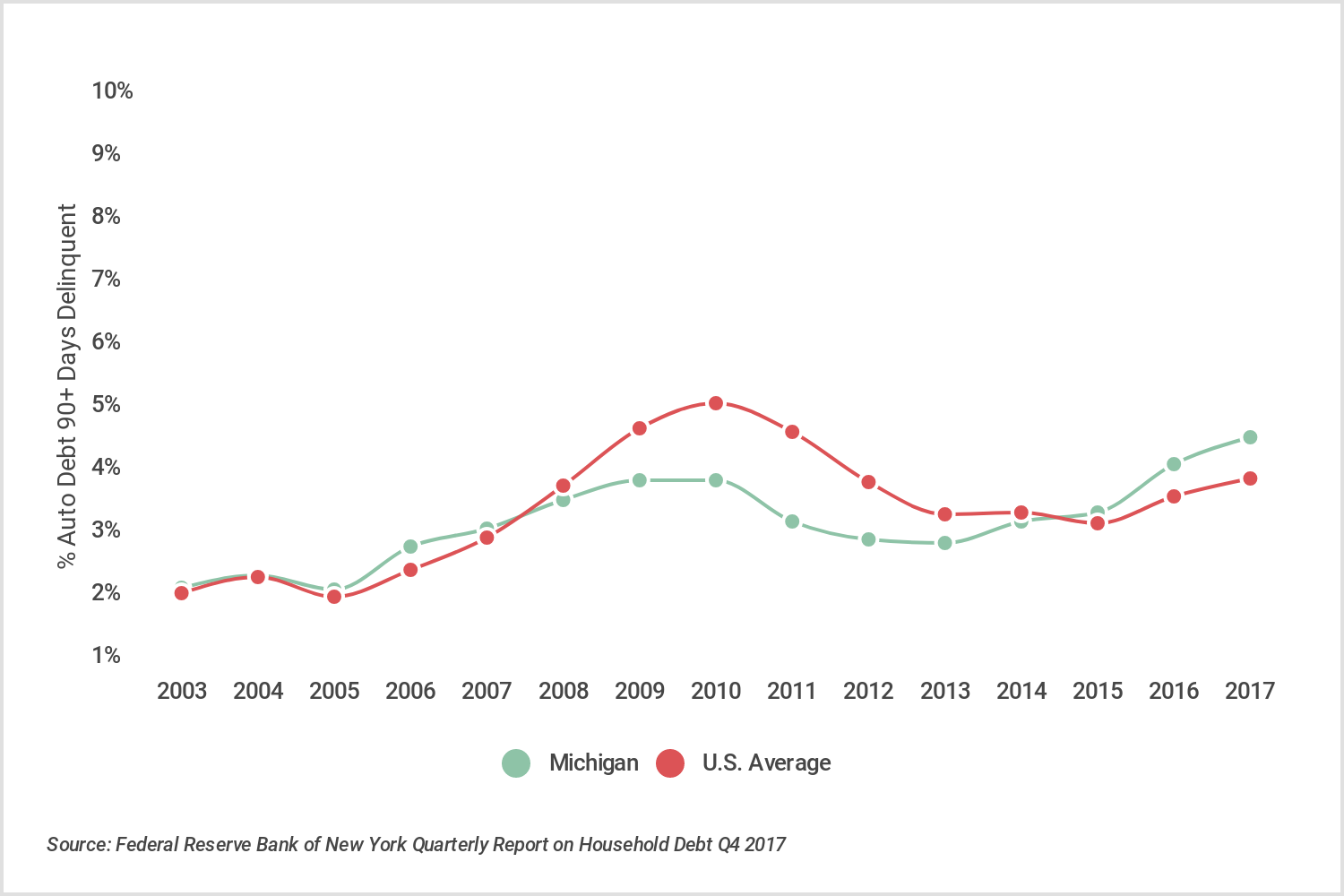

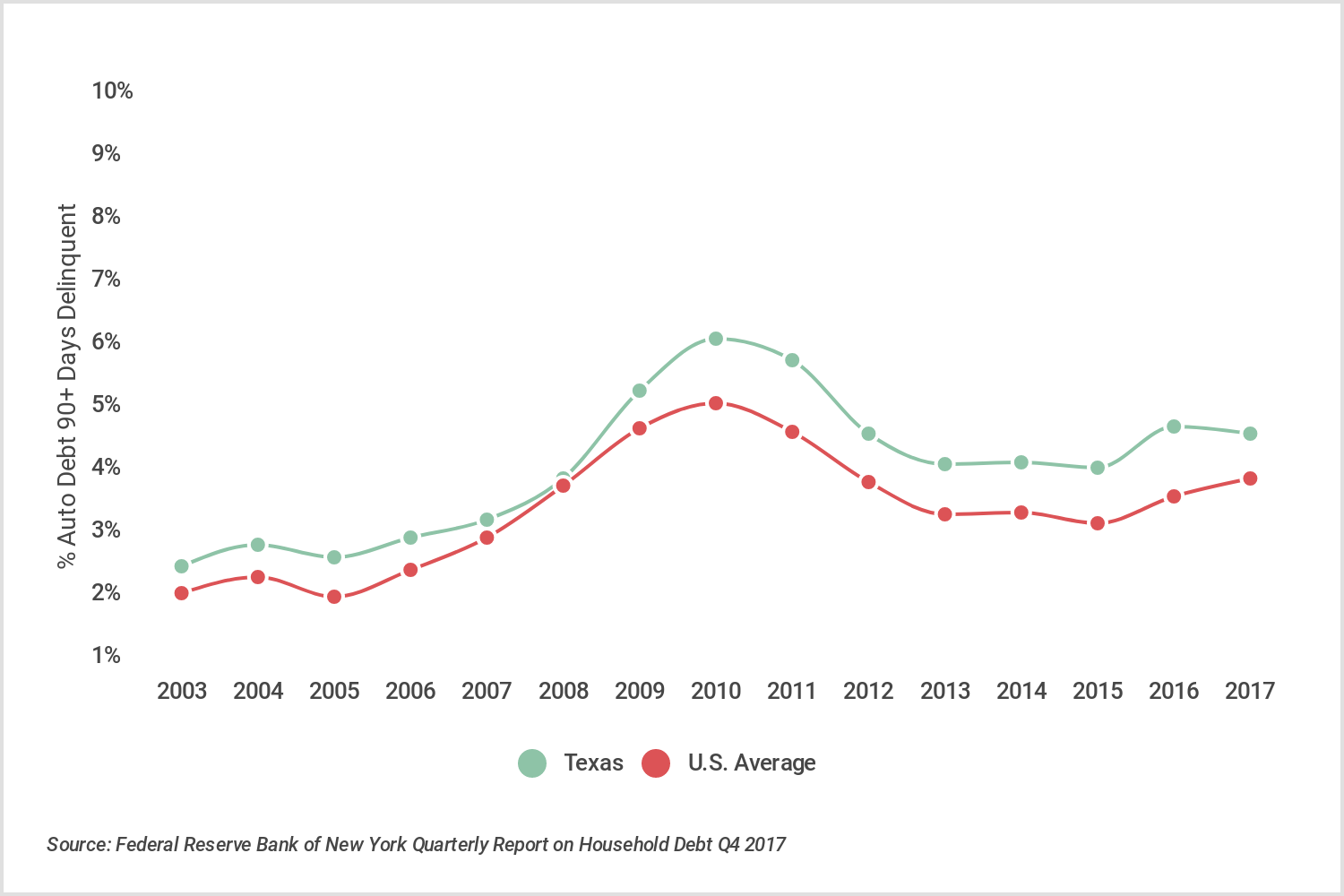

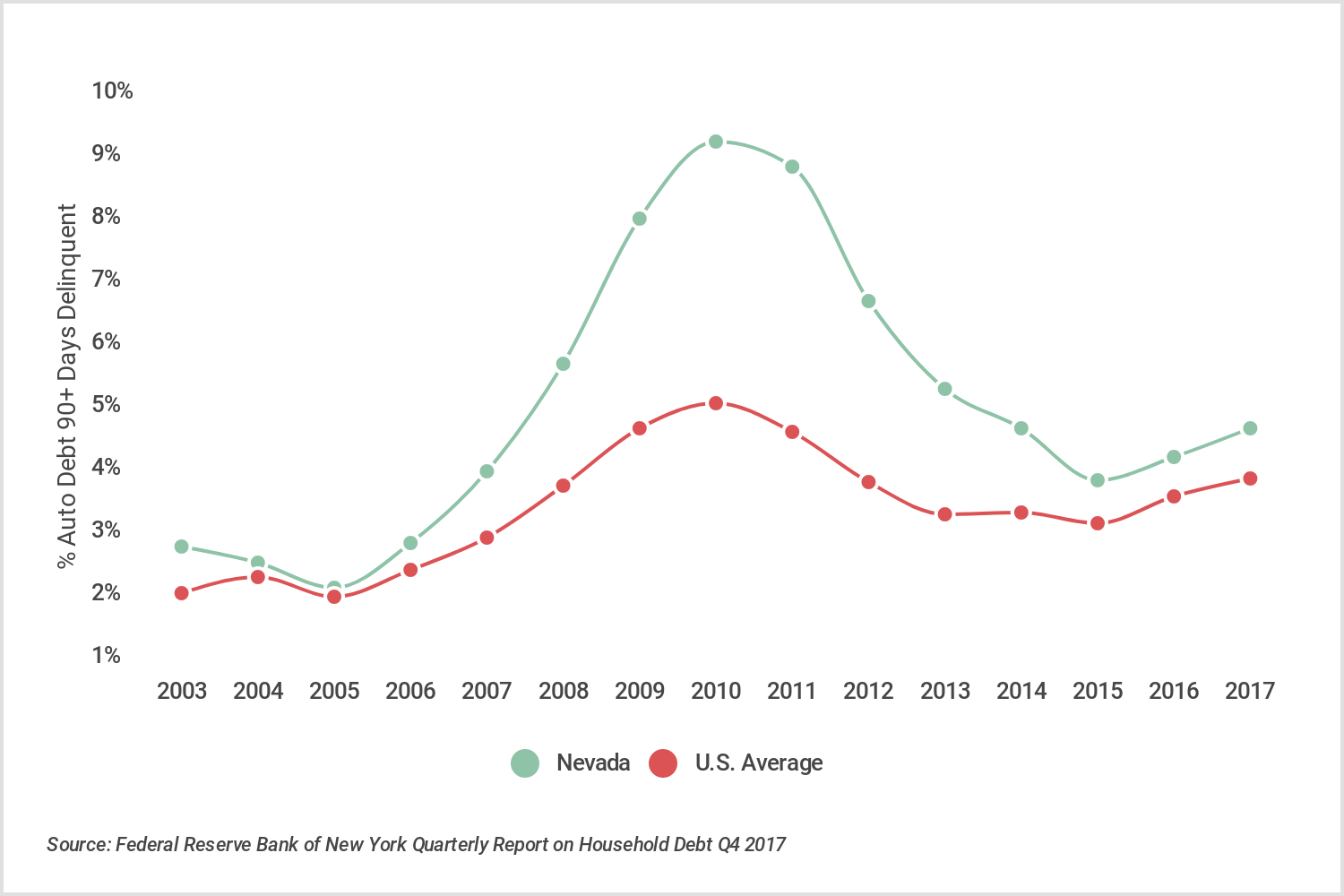

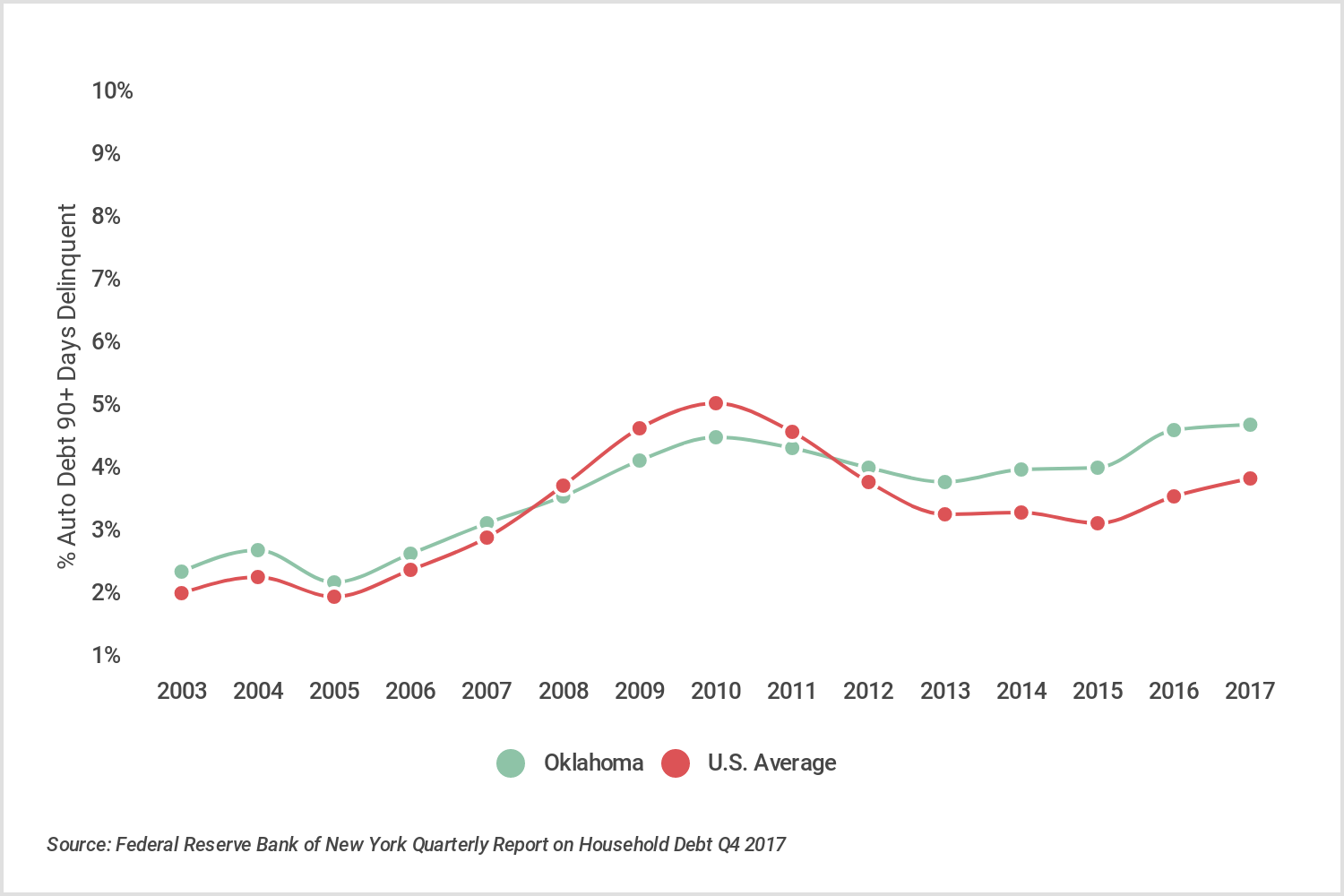

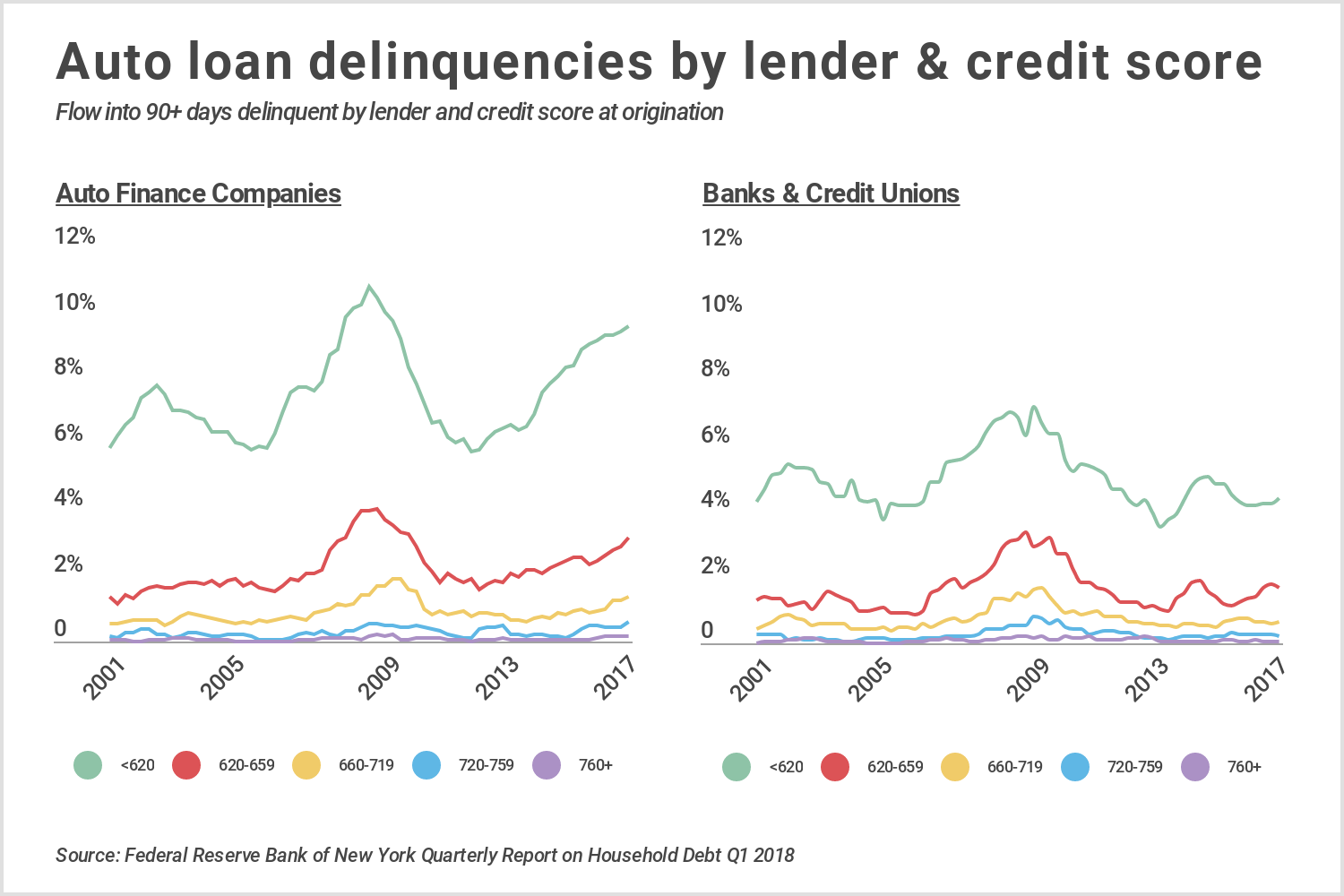

Relaxed borrowing requirements have correlated with rising auto loan delinquencies. In Q1 2018, the percent of total auto loan balances 90+ days delinquent continued its three year upward trend, reaching 4.26 percent, a rate that experts believe actually understates the severity of the problem. While delinquency rates for loans originated by banks and credit unions have been steadily improving since the recession, those for loans originated by auto finance companies—particularly among subprime borrowers (below 620 credit score)—have increased sharply.

This sharp rise in delinquencies in an otherwise strong economy suggests that some lenders are letting consumers purchase more car than they can afford, which later puts them in a position of financial distress. Especially when it comes to car loans, a default can put the borrower in a vicious cycle that is difficult to recover from. Apart from the immediate impact that a default has on a person’s credit score, not having access to a vehicle can reduce earnings, which ultimately affects the ability to pay off other outstanding debt.

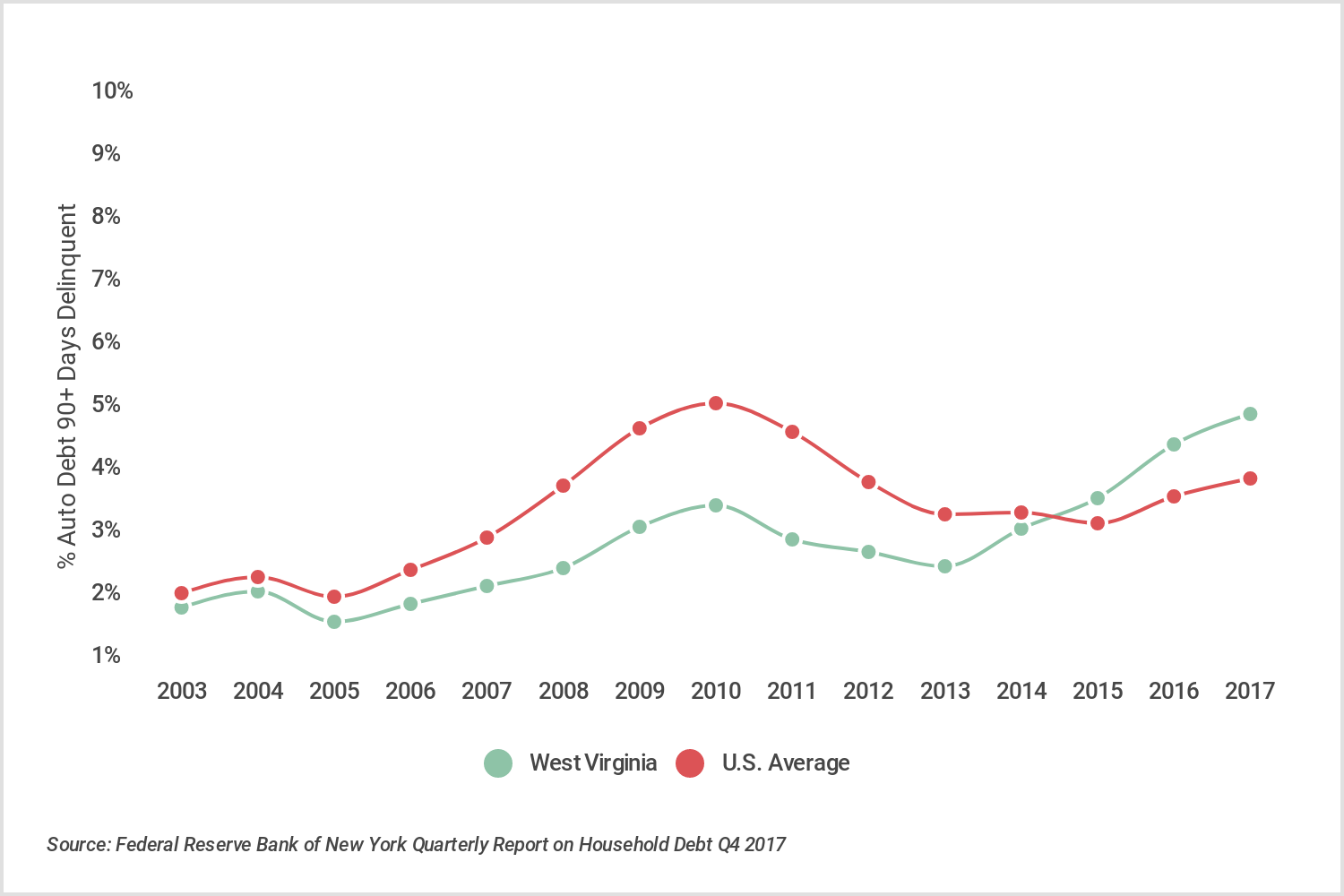

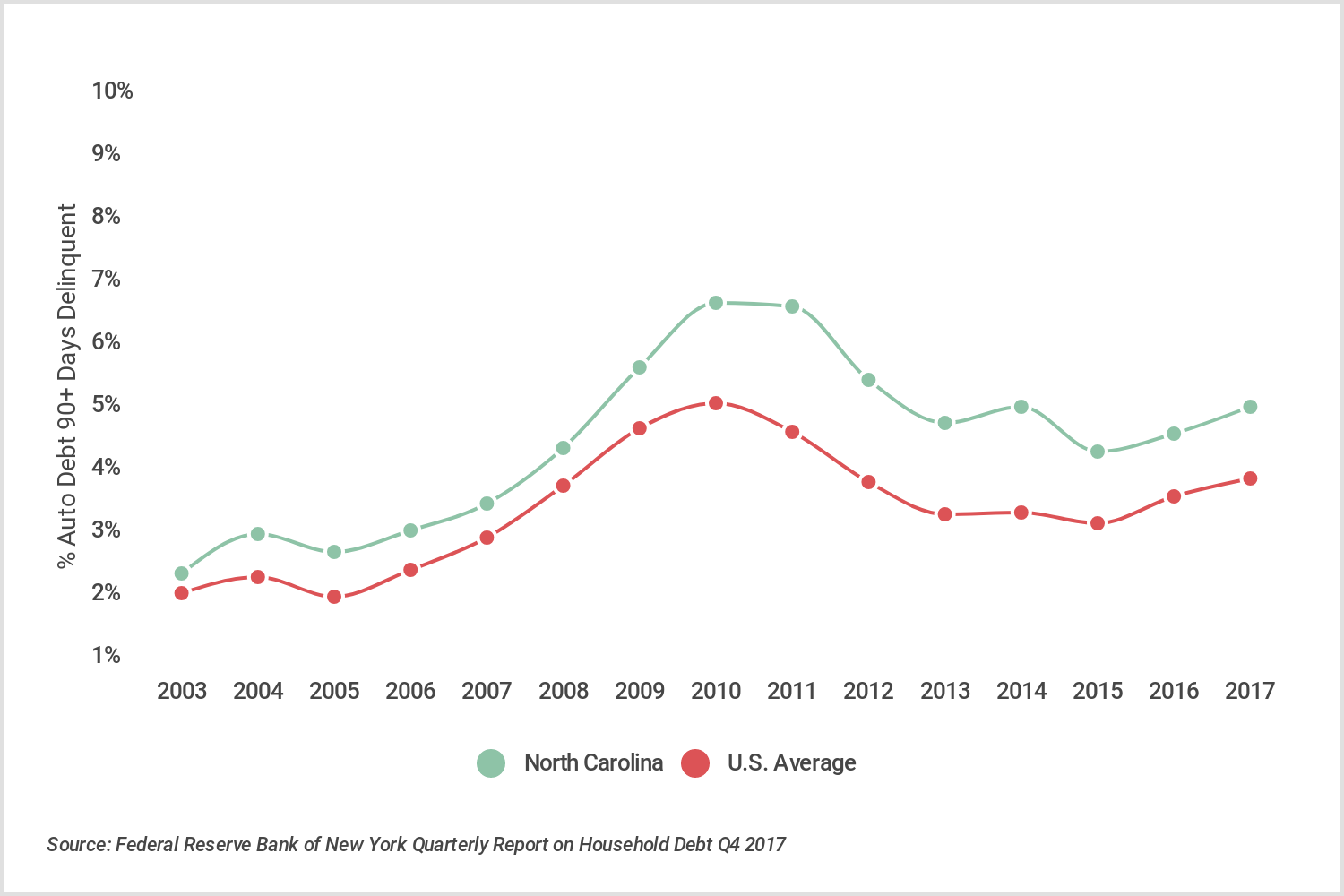

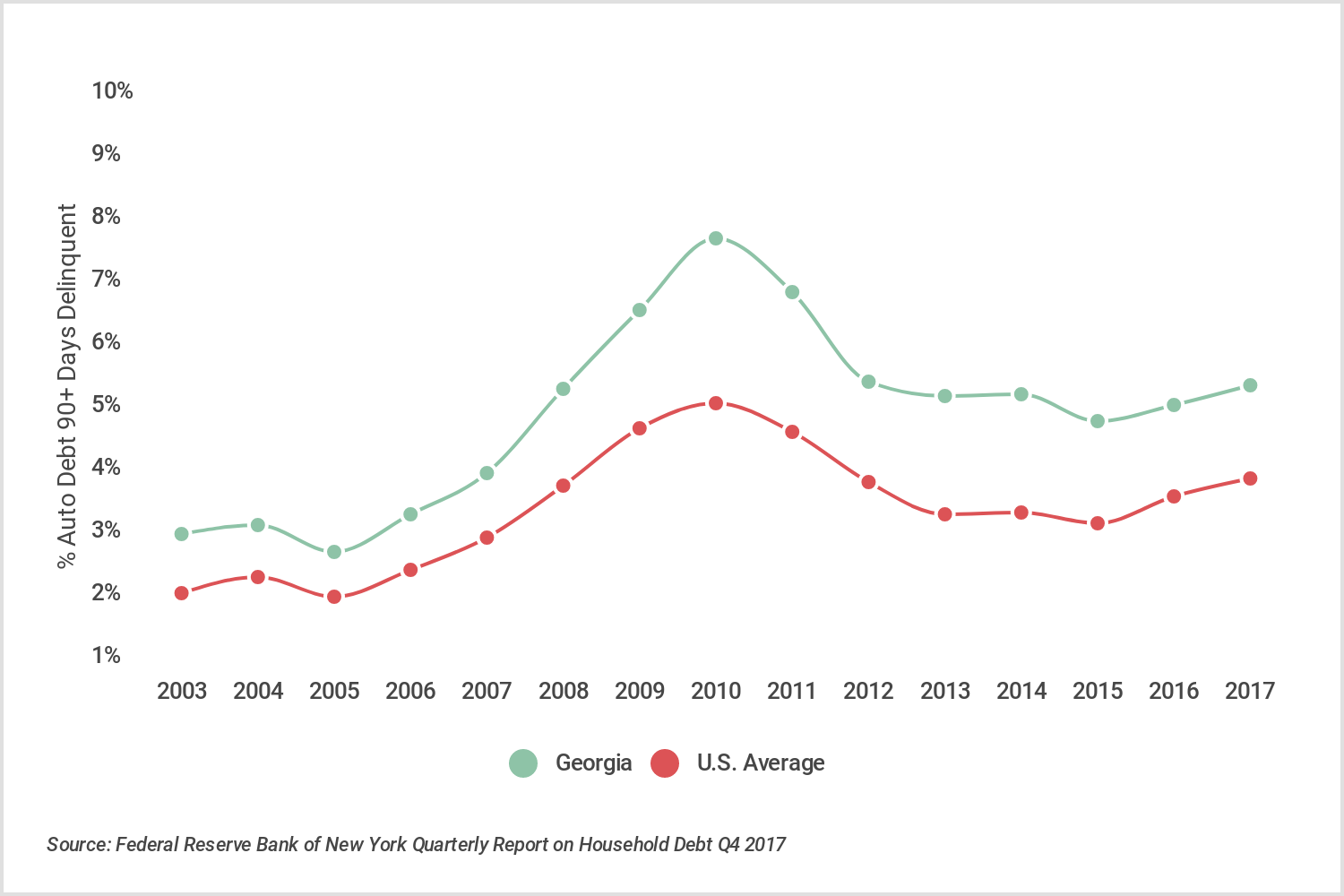

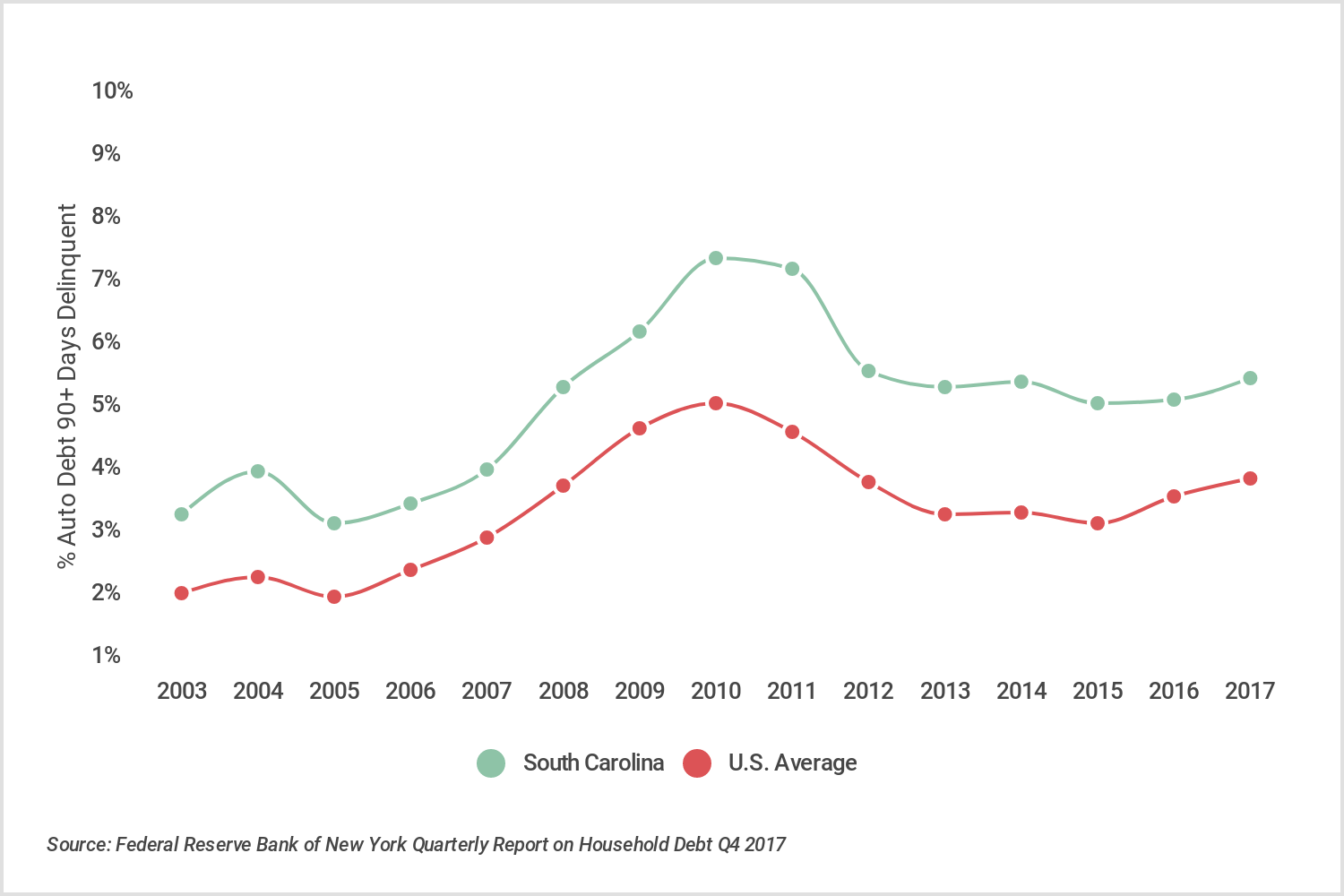

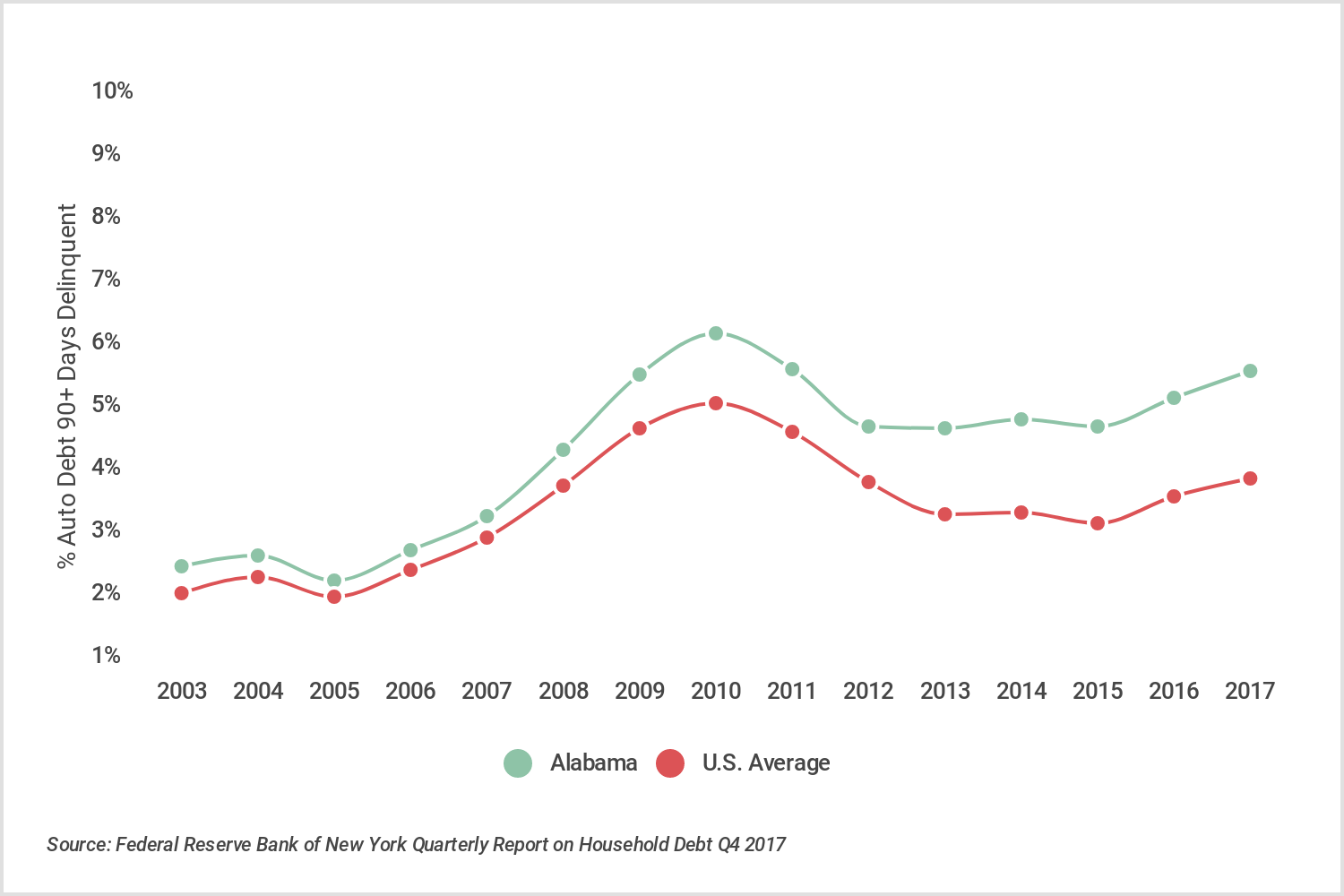

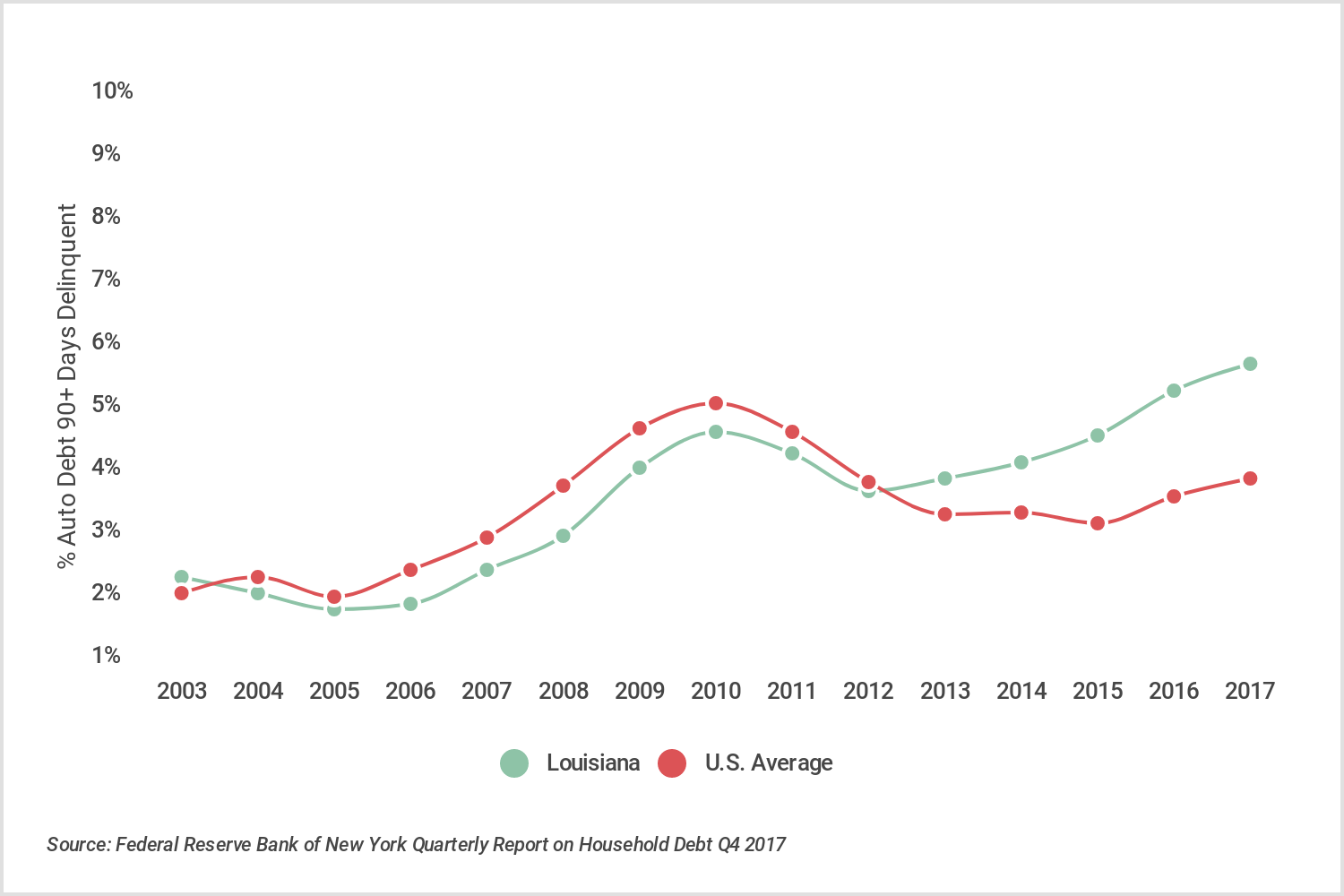

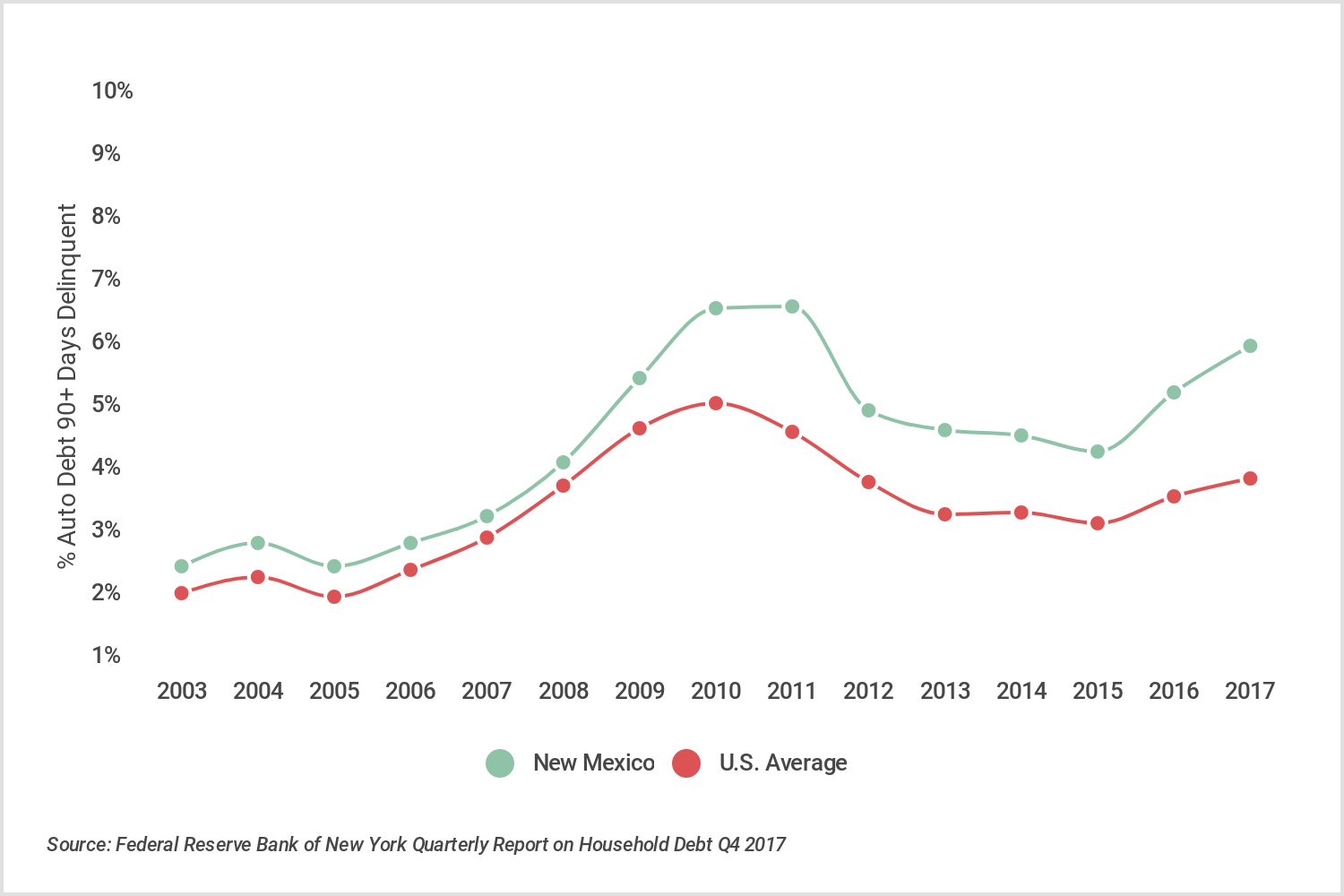

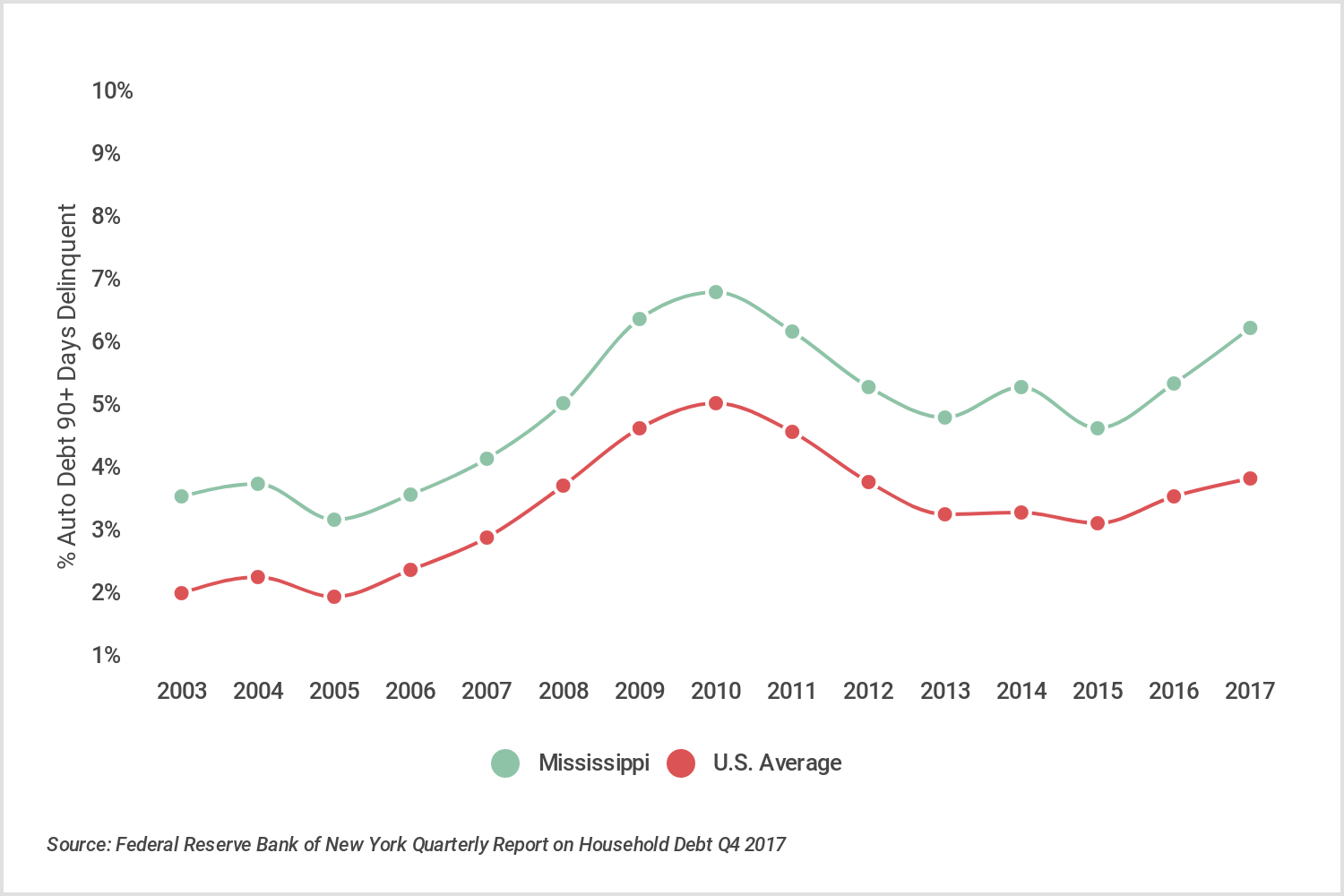

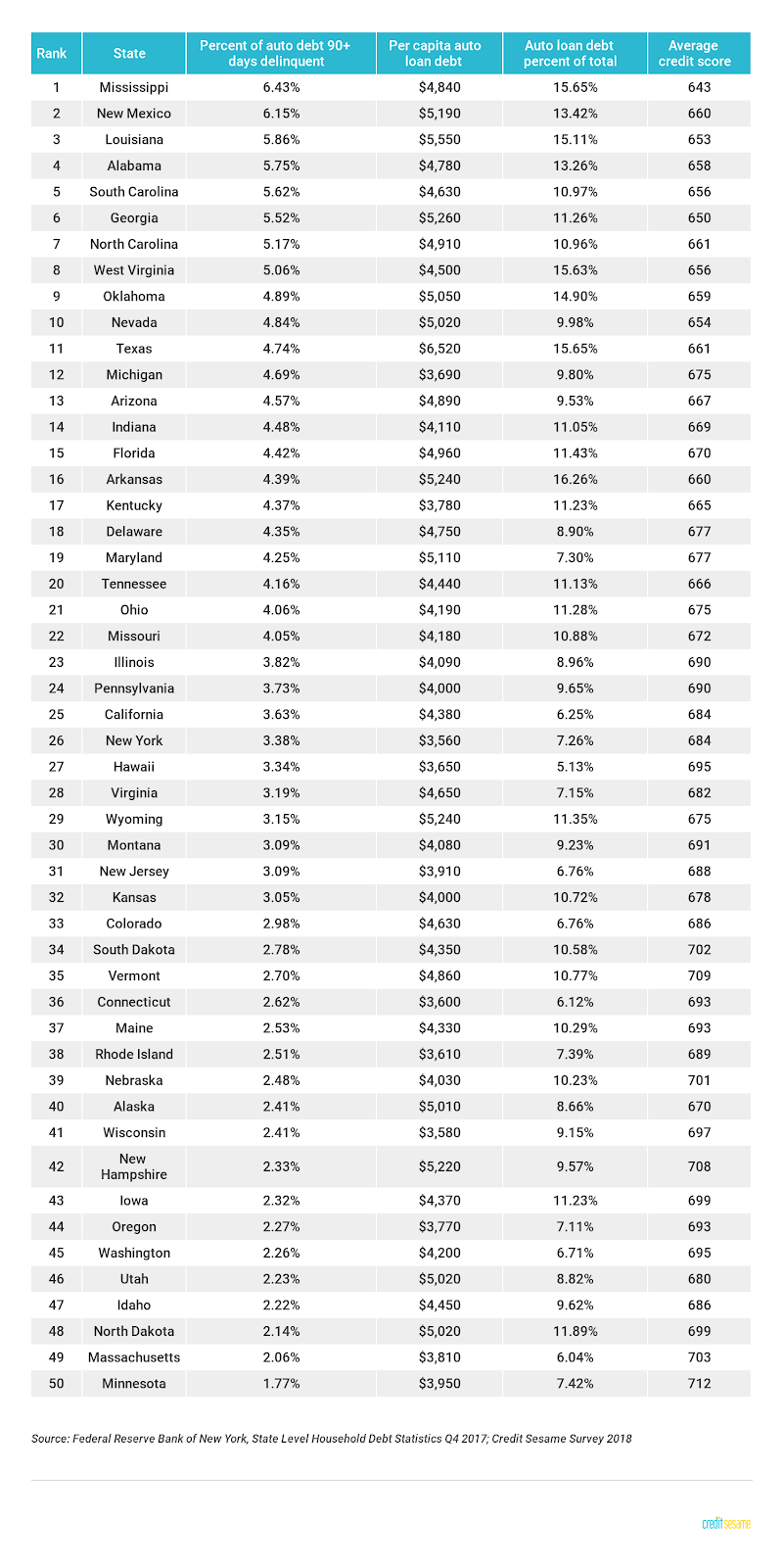

Despite rising auto loan debt nationally, not every state shows the same trend. To see which states have been most impacted, credit management platform Credit Sesame analyzed the most recent New York Fed data. Its researchers found the following:

- Auto loan delinquencies are more prevalent in southern states than northern states.

- Comparing states, auto loan delinquency is not correlated with per capita auto loan debt; but rather, it shows a positive correlation with auto loan debt as a percent of total debt. In other words, it’s not how much overall auto loan debt a state carries that predicts delinquencies; instead, it’s how much auto loan debt relative to total debt.

- Auto loan delinquency shows a strong negative correlation with average credit score. States with lower average credit scores are more likely to have high delinquency rates.

Here are the top 20 states with the most auto loan debt: