Second of a two-day series

In August 2004, Moody's Corp. unveiled a new credit-rating model that Wall Street banks used to sow the seeds of their own demise. The formula allowed securities firms to sell more top-rated, subprime mortgage-backed bonds than ever before.

A week later, Standard & Poor's moved to revise its own methods. An S&P executive urged colleagues to adjust rating requirements for securities backed by commercial properties because of the "threat of losing deals."

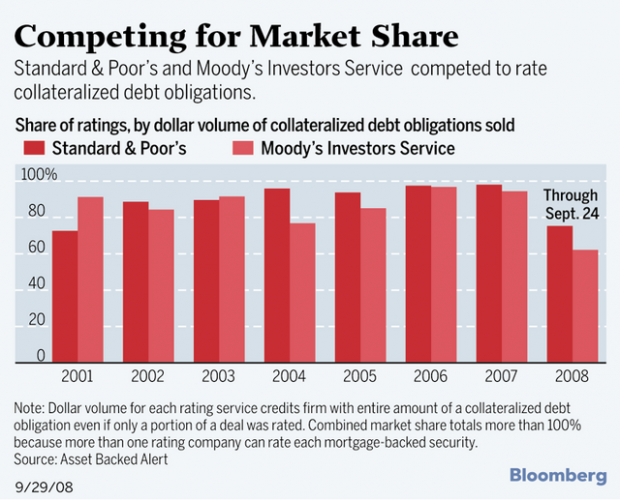

The world's two largest bond-analysis providers repeatedly eased their standards as they pursued profits from structured investment pools sold by their clients, according to company documents, e-mails and interviews with more than 50 Wall Street professionals. It amounted to a "market-share war where criteria were relaxed," says former S&P managing director Richard Gugliada.

People are also reading…

"I knew it was wrong at the time," says Gugliada, 46, who retired in 2006 and was interviewed in May near his home in Staten Island, N.Y. "It was either that or skip the business. That wasn't my mandate. My mandate was to find a way."

Wall Street underwrote $3.2 trillion of loans to home buyer with bad credit and undocumented incomes from 2002 to 2007. Investment banks packaged much of that debt into investment pools that won AAA ratings, the gold standard, from New York-based Moody's and S&P. Flawed grades on securities that later turned to junk now lie at the root of the worst financial crisis since the Great Depression, says economist Joseph Stiglitz.

"Without these AAA ratings, that would have stopped the flow of money," says Stiglitz, 65, a professor at Columbia University in New York who won the Nobel Prize in 2001 for his analysis of markets with asymmetric information. S&P and Moody's "were trying to please clients," he said. "You not only grade a company but tell it how to get the grade it wants."

SEC places some blame

The Securities and Exchange Commission in July identified S&P and Moody's as accessories, finding they violated internal procedures and improperly managed the conflicts of interest inherent in providing credit ratings to the banks that paid them.

S&P and Moody's earned as much as three times more for grading the most complex of these products, such as the unregulated investment pools known as collateralized debt obligations (CDOs), as they did from corporate bonds. As homeowners have defaulted, the raters have downgraded more than three-quarters of the AAA-rated CDO bonds issued in the last two years.

Facing the threat of lawsuits and tighter regulation, Moody's and S&P now say they are adopting tougher requirements to more accurately evaluate and monitor debt.

Starting in 1996, Moody's used a framework known as the binomial expansion technique for rating CDOs — structured funds consisting of aircraft leases, franchise loans, high-yield bonds, hotel mortgages and mutual-fund fees. On the theory that diversification reduced risk, the BET formula rewarded balanced portfolios and punished concentrations of assets.

On Aug. 10, 2004, Moody's managing director Gary Witt introduced a new CDO rating method that dispensed with the diversity test and made other adjustments to the evaluation of structured-finance products.

As a tradeoff, bankers got more flexibility, says Jeremy Gluck, 52, a former Moody's managing director, who worked with Witt. "They could put together a deal with greater concentrations in one area or another." In September 2005, Witt and colleagues published a follow-up analysis. Compared with the BET, the new model now projected that the likelihood of collateral defaults affecting CDO bonds rated at least Aa could be 73 percent lower.

"The effect that had on structures was to create more Aaas," says Thomas Priore, 39, chief executive officer of Institutional Credit Partners LLC in New York, which oversees $13 billion of fixed-income investments.

Underwriters made obtaining a top grade from one or both raters a condition for the sale of the investment pools.

The reckoning swept Wall Street in 2007. On July 10, Moody's cut its grades on $5.2 billion in subprime-backed CDOs. That same day, S&P said it was considering reductions on $12 billion of residential mortgage-backed securities.

Still, they continued stamping out AAA ratings.

"The greed of Wall Street knows no bounds," says Stiglitz. "They cheated on their models. But even without the cheating, their models were bad."