The second round of stimulus checks from the US government are going out this week. Business Insider reports the checks will pay up to $600 each, or $1,200 per married couple, plus additional funds for children. According to Congress's bill authorizing the payments, most of the direct cash payments will be sent to qualifying Americans by January 15. To track your payment, visit the 'Get My Payment' section of the IRS website at www.irs.gov/coronavirus/get-my-payment Direct deposits and paper checks are arriving this week.

Parents of babies born between Jan. 1 and Dec. 31, 2020, may be eligible for $1,100 in extra stimulus money, according to an MSN report.

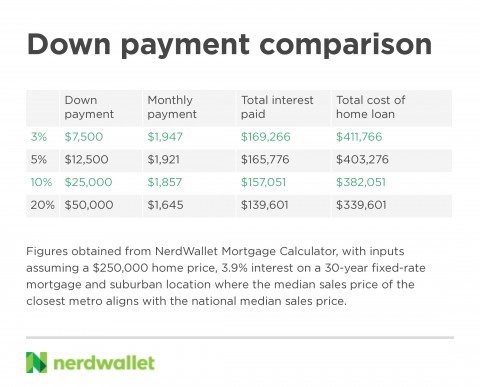

Here’s how it works:

The two rounds of stimulus checks are considered advancements of the 2020 tax credit, with most people receiving payments before filing taxes for the year, as MSN reports. Instead of waiting until citizens filed their 2021 taxes to hand out the tax credit, the IRS is pushing out those tax credits immediately due to the urgency of the pandemic.

According to MSN, the IRS is looking at tax returns from 2019 to determine eligibility (and 2018 returns for the first round of payments).

So parents who gave birth to a child in 2020 may be eligible now for the tax credit for both stimulus checks, if they meet the income limitations. This means these parents could get $500 additional from the first stimulus and $600 additional from the second stimulus, adding up to $1,100 total in additional stimulus payments.

People are also reading…

Tax returns for 2019 are being used to determine the stimulus checks. Hence, the IRS won’t know about your 2020 baby or adopted child (the same applies to children who were adopted in 2020).

Parents will need to file their 2020 tax return and get the $1,100 in additional stimulus money as a refund recovery credit, according to MSN.

The government started sending out $600 stimulus checks on Dec. 29, 2020. U.S. citizens can use the IRS’ tool “Get My Payment” to see when their second stimulus will arrive.

A number of taxpayers who use tax preparation services, such as H&R Block and TurboTax, say their second relief payments were sent to the incorrect bank account, forcing them to wait longer for their money. Read more about that here:

How the IRS knows if you cheat on your taxes, and more answers to your personal finance questions

How the IRS knows if you cheat on your taxes

Mailboxes are flooded with tax forms every year around this time, and many of them can be confusing, feel unnecessary or involve seemingly trivial amounts of money. But before succumbing to the urge to shove those pieces of paper into a drawer and pretend they don’t exist, beware — the IRS probably already knows what’s in that drawer. Two tax pros explain.

Double trouble

Many tax forms you receive at tax time don’t go only to you; in many cases, the senders give copies to the IRS as well. Those forms, called information returns, typically are records of certain payments you received or made during the tax year that you usually need to report on your tax return. Some of the most common information returns are W-2s, which report wages earned from a job, and 1099s, which report money received for things such as freelance work, dividends or interest.

But other money moves you make could put information returns in the IRS’ mailbox, too, says Ignatius Jackson, a certified public accountant in Phoenix. Distributions from retirement accounts could generate an information return, for example, as could unemployment compensation, prizes or awards, college fund withdrawals, stock transactions or canceled debt. Even paying your mortgage can generate one.

Meeting your match

Why the copies for all of these? The IRS uses information returns to double-check you. “What the IRS will do once you file your tax return, whether you’re e-filing or filing on paper, they go ahead and match up what’s in their system of records and compare that to what you have on your return,” Jackson says. “If there’s a difference between the two, they’ll usually send you a letter saying, ‘Hey, we have a different amount. We show that you had more income than what you reported. You owe us some additional money. If you disagree, respond and let us know why. What has been reported to us is incorrect.’”

Donna Mullin, a certified public accountant and director at Boyer & Ritter in Camp Hill, Pennsylvania, says she’s seen clients get notices for very small amounts. But two things can help avoid the headache, she says.

Check your information returns for accuracy

If your employer sends you a W-2 that says you earned more than you actually did, don’t ignore it or report a different number on your tax return. “The best thing for you to do if you get a wrong one is to contact the issuer — the person who gave it to you — and ask for correction,” Mullin says.

“It’s awfully hard to prove you didn’t have that income if somebody else says you did.”

If after you file your taxes an unexpected information return lands in your mailbox or you find one you shoved in a drawer weeks ago, you can get a do-over by filing IRS Form 1040X to amend your tax return, Jackson adds. And avoid foot-dragging. “The best thing would be to file an amendment before you receive the letter,” he says.

Don’t automatically assume you screwed up

If the IRS sends a bill for more taxes and claims you owe because its records don’t match the return you filed, take a minute to review everything carefully before busting out the checkbook. “A lot of people just pay it when in fact they don’t necessarily owe the money,” Mullin says. “I would not assume that it is right and you were wrong. I would assume that you could be right. You have to read the details to see what they think you didn’t report and look at your return and see if it’s actually on there.”

Often the issue is that something on your tax return is labeled slightly differently than what’s on the information return, she says. “In more cases than not, certainly if the return’s professionally prepared, the IRS is wrong, but the matching’s just not working perfectly,” Mullin says. “Nine times out of 10 they’re wrong; we’re right. We just have to just help them to locate the match.”

3 reasons to pay for spring break with a travel credit card

It may be cold outside now, but spring is just around the corner. A recent NerdWallet survey found that 33% of Americans plan to travel for spring break vacation this year — if you’re in this camp, now’s the time to make travel plans for spring break (if you haven’t already).

The same survey, conducted online by The Harris Poll of over 2,000 U.S. adults, found that those planning to go on a 2020 spring break trip expect to spend $1,488, on average, on their vacation. Surprisingly, only 33% of those planning to travel for spring break this year plan to use a credit card for some or all of those costs.

Given that many travel credit cards offer 2 points or more per dollar on travel spending, anybody who doesn’t charge their spring break expenses to a card like this is missing out on thousands of points.

To put it in perspective: If a third of Americans will spend $1,488 on spring break travel and only a third of them will pay with a credit card, that amounts to over 200 billion missing points from the other two-thirds. Yes, that’s billion with a “b.”

Of course, not everybody can or should pay for travel with a credit card. Those with poor credit or who are already carrying credit card debt shouldn’t make their situation worse by adding a big travel bill.

For those in good financial health, here are three reasons to book spring break travel with a credit card:

1. You can earn points

This is the most basic reason to book any flights and hotels with a travel card, but it bears repeating.

Similarly, airline and hotel cards only offer big spending bonuses for booking on their specific airline or hotel. If you’re an advanced credit card wielder, you can book each part of your spring break excursion with the appropriate card, or you can just use a catch-all travel card to cover all your expenses. Either way, you’re doing better than 66% of fellow spring breakers who won’t be earning points at all.

2. Your trip could be protected

Some travel credit cards, especially the premium ones with high annual fees, offer various trip protections for travel purchased through the card.

These benefits generally apply only in case of unforeseen consequences. If you cancel your spring break travel last-minute for personal reasons, they won’t help you. But they can help make the difference between a disaster and an inconvenience.

3. You can avoid bag fees and improve your travel experience

Your travel credit card may come with other perks that can help you travel more comfortably or save cash. Here are a few:

- A card with Global Entry or TSA Precheck perks can make your airport experience less stressful (some cards reimburse at least part of your enrollment fees).

- Some airline credit cards offer free checked bags, priority boarding and discounts on in-flight purchases.

- Having a credit card with airport lounge access can save you some money on food and drinks at the airport while providing a comfortable place to wait for your flight.

- A card with top-notch rental car coverage helps protect you in case of theft or damage to your rental.

The bottom line

Yes, spring break for many is all about intentionally making bad decisions. But an extra shot of tequila is one thing; missing out on the benefits of booking with a credit card is quite another.

Whether for the points, trip protection or free bags, your future self will thank you for the wise decision — even if your liver doesn’t.

This survey was conducted online within the U.S. by The Harris Poll on behalf of NerdWallet from Feb. 4-6, 2020, among 2,031 U.S. adults ages 18 and older, including 626 who are planning to travel for spring break vacation in 2020. This online survey isn’t based on a probability sample and therefore no estimate of theoretical sampling error can be calculated. For complete survey methodology, including weighting variables and subgroup sample sizes, contact Mauricio Guitron at mguitron@nerdwallet.com.

Stop stressing: You don’t need a 20% down payment to buy a home

Many Americans may be unnecessarily talking themselves out of homeownership. Thirty-seven percent of nonhomeowners say not having enough saved for a down payment is holding them back from homeownership, but 62% of Americans incorrectly believe you have to have at least 20% of a home’s purchase price to buy, according to NerdWallet’s 2020 Home Buyer Report.

“These days, you don’t need to put a full 20% down on a home,” says NerdWallet home and mortgage expert Holden Lewis. “Lenders offer mortgages with far less — as little as 3% down — which allows far more people to get into homeownership sooner.”

So, how do you know just how much you need to save up based on your specific goals? It requires a little strategizing.

Before you can zero in on a down payment target, you have to determine how much home you can afford and when you’d like to start home shopping. First, set your homebuying budget with a home affordability calculator to get estimated monthly payments based on various home prices, down payment amounts and locations.

Then, set an approximate timeline. Maybe you’re planning a wedding and know you won’t be ready to purchase for at least two years, or you’re just starting a graduate program and want to give yourself five years to find employment and settle down after graduation. Be realistic and account for your life circumstances.

With a homebuying budget and estimated timeline, you can start running numbers to set a down payment savings goal.

1. Is saving 20% by your goal date realistic?

Calculate 20% of that homebuying budget and determine if it’s feasible to stash that amount away in the time you’ve allotted.

If the answer is yes, great! A big down payment doesn’t only lower monthly payments, it can save you thousands of dollars in interest over the life of the loan and eliminate the need to pay private mortgage insurance.

If it’s no, you have two options: Revisit your goal parameters — opting for a less expensive home or pushing out your target date — or consider a smaller down payment.

Example: For a $250,000 home, someone starting with $0 saved would need to save about $1,400 each month to reach a 20% down payment in three years. For most folks, that’s a stretch. Adjusting the timeline to five years would require monthly savings of about $800. While that may be more realistic, a smaller down payment could get you in a home sooner and with less stress to your monthly household budget.

2. How much can you save by your deadline?

What’s the most you can save monthly for your down payment goal? If you don’t already know the answer, create a monthly household budget to help figure out where your money is going and how much you can set aside.

At a high level, allocating 50% of your post-tax income toward your needs, 30% toward your wants, and 20% toward savings (including your down payment) and debt repayment is a sustainable approach. But by accounting for all of your income and spending, you may realize you can sacrifice a little of your dining out and entertainment money (wants) temporarily to make homeownership a reality sooner.

Example: You decide you can set aside $350 each month. If you’re still hoping to start home shopping in three years, this would leave you with $12,600, or a 5% down payment. Because many lenders accept down payments of 5%, and even lower, you’ll be in a good place to buy around your three-year target date.

3. Do you qualify for down payment assistance?

Such programs can both shorten the path to homeownership and free existing savings for closing costs, moving or other homebuying expenses.

Weighing the trade-offs of a high vs. low down payment

A down payment doesn’t have to stand in the way of homeownership. Smaller down payments and down payment assistance programs can help you achieve your homebuying dreams more quickly and leave you some savings for an emergency fund or unexpected repairs.

It’s worth considering, too, since there’s no guarantee your $250,000 homebuying budget will get you the same type of property in three years as it would if you bought sooner. Home prices have been rising, but what will happen in the future and what it could mean for your down payment target is hard to know.

How much of a down payment you need is ultimately a personal decision, a balancing act between financial factors and how quickly you want to achieve your dream of homeownership.