Over the past few years, credit card balances were paid down and delinquent accounts became less common. But two years after the COVID-19 pandemic began, those trends — spurred by increased savings and relief programs — could evaporate, especially as inflation soars.

The pandemic economy unexpectedly changed many households’ finances for the better — personal savings increased and debt decreased. Now, however, inflation is high, inflows like the advanced child tax credits and expanded unemployment benefits have ended, kids are back in child care, and parents have returned to the office. The money habits we had in 2020 and 2021 likely won’t last. Here’s a look at how credit card usage in particular has changed and how people can protect their credit as personal finances stand to shift again.

Cardholders used less of their limits

Over the past decade, credit card balances hovered at about 23% to 24% of their limits, according to data from the Federal Reserve Bank of New York. But in the second quarter of 2020, they dropped to 21%. This seems like a modest dip, but that difference of 2 to 3 percentage points is considerable when you’re talking about hundreds of billions of dollars in total debt.

People are also reading…

It was the first time since at least 1999 that credit card balances were at 21% of their limits. They hit 20% in the first three quarters of 2021.

Falling utilization can happen because of higher credit card limits, lower balances or a combination of the two. During this period, lower utilization was mostly due to lower balances.

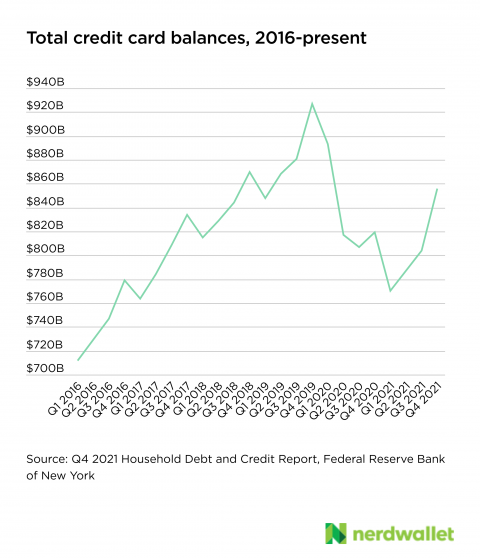

Balances also fell

Nationwide, credit card balances have typically totaled roughly $800 billion over the past five years, according to the New York Fed. From the first quarter of 2020 to the first quarter of 2021, credit card balances fell nationally by $123 billion, or nearly 14% — the biggest single-year drop since 2001.

Those national balances rose in the third and fourth quarter of the past year, but the end of the year has come with credit card balance increases in each of the past five years, as spending rises toward the holiday season. When data for the first quarter of 2022 is released in coming weeks, it will indicate whether this most recent jump was seasonal or the start of a more sustained climb.

At the state level, per capita balances fell across all 50 states and Washington, D.C., from the end of 2019 to the end of 2021. They dropped the furthest in California, Hawaii, Oregon and Rhode Island, where they fell 13% during this period. View all state-level per capita balances here.

Fewer accounts moved into delinquency

The share of newly delinquent credit card accounts began falling in the second quarter of 2020, when the pandemic was getting into its early full swing. This downward slope has continued since. As of the last quarter of 2021, it stood at 4.1%, the lowest in at least 18 years, according to the New York Fed.

Furthermore, the share of credit card accounts being charged off — when a bank writes off a seriously delinquent debt as uncollectible — has fallen below 2% for the first time since at least 1985, according to data from the St. Louis Fed.

The drop in delinquent accounts has not been unique to credit cards, however. Programs designed to buffer potential household economic effects of the pandemic — such as mortgage forbearance and student loan payment pauses — meant that the share of total debts going into new delinquency likewise began falling in the first half of 2020, hitting an 18-year low of 1.9% in the third quarter of 2021.

What might reverse these positive trends

Pandemic relief programs such as rental assistance, mortgage forbearances, advanced child tax credits and stimulus payments all contributed to Americans saving more. This increase in personal savings meant having more money to pay for goods and services outright, and more money to pay down debt. But as these programs have subsided, so has the personal saving rate. As a result, many credit card holders will likely soon find themselves in situations similar to where they were before the pandemic began. Having paid off some credit card debt can make managing household finances easier only if cardholders are able to keep that debt off.

Perhaps the biggest thing working against lower credit card balances and up-to-date accounts is inflation.

In response to expected rising prices, some people may feel compelled to make big-ticket purchases now to avoid spending more on them at a later date. At the other end of the spectrum, consumers with less discretionary income will feel a pinch from rising prices. With the cost of food, gasoline and nearly everything else eating into a finite amount of money on hand, credit cards may once again be a lifeline.

Managing credit cards in 2022 and beyond

The ability to stick to good credit use habits may ebb and flow over the years — particularly in the face of household and global economic turmoil — but keep these best practices in sight as a goal.

Don’t spend more than you can pay off in a single month

Paying off your balance each month keeps your credit healthy, perhaps even “excellent” according to the credit bureaus’ systems. The myth that you have to carry debt to keep improving your credit is just that, a myth.

And carrying a balance from month to month racks up interest charges quickly. For example, amassing $2,000 in credit card debt and only making a minimum payment would cost about $2,870 in interest, on average — more than doubling the cost of what you purchased — and take more than 16 years to pay off.

Keep utilization under 30%

Having a balance higher than 30% of your limit on any card or across all your accounts can damage your credit, not to mention make it difficult to pay off if life throws something like a job loss your way.

If you hit a wall, make at least the minimum payment

In times of financial strife, you may struggle to pay off your credit card balance in full. In these instances, making only the minimum payment is perfectly acceptable. Though paying the minimum can be a recipe for hundreds if not thousands of dollars in additional interest, small payments are better than no payments at all.

Know when (and where) to find help

If the minimum payment on your credit card(s) becomes unmanageable, the first place to turn is your card issuer. More than 1 in 20 Americans were on a credit card hardship program between March 2020 and November 2021, according to NerdWallet’s annual Household Debt analysis. But credit card hardship programs are not only a pandemic relief program. They are designed to help people who are experiencing difficulty paying their bills due to many types of issues — unemployment, illness and natural disasters, for example.

If you continue to struggle with your debt load, consider a credit counseling or debt management program. Many of these programs are free and can help you set up a plan to get your debt under control, or guide you through the option of filing for bankruptcy.

___

Check out this week's best personal finance reads:

Did you know April is Financial Literacy Month? Host Teri Barr is talking with Kimberly Palmer, Personal Finance Expert with NerdWallet, to learn why it's a good time to start caring about your financial health!

8 tactics to break credit card debt cycles

1. Reflect on spending habits

Maybe you ditched debt, but history can repeat if you don’t unpack the motivations that contributed to it. A get-out-of-debt plan that works in the short term may not be sustainable over the long term if it doesn’t align with your priorities, according to Julia Kramer, a financial behavior and leadership consultant at Signature Financial Planning in Pennsylvania.

Kramer suggests tracking transactions dating back a week or more. Add a plus sign next to those purchases you’re willing to repeat and a minus sign next to those you’re not. For obligatory purchases like gas and groceries, add an equal sign.

Note the date, the item purchased, the amount and the need the purchase met. Those frequent lattes or meals out with friends may be more about the personal connection experienced, or something else, as opposed to the gratification provided by the item, according to Kramer.

This information is key to identifying areas in your budget that are negotiable. For example, you may be more willing to choose budget-friendly food in order to keep a facial that meets an internal need for self-care and connection, Kramer says.

If your spending strays upon experiencing feelings like anxiousness or boredom, make a plan for those occasions. It might mean budgeting extra money or employing tricks like using a credit card lock feature to prevent spending.

2. Use cash for certain categories

If you want to reel in spending on categories like dining out or entertainment, for example, set aside physical cash to stay within budget. Money in hand can lead to more mindful spending, according to Kramer.

3. Track spending

Create a tracking system that works for you. Setting up spending alerts on a credit card account can notify you if purchases exceed a certain amount. Tracking spending with a spreadsheet, bullet journal or budgeting app, for instance, can also help with mental accounting.

“I would not open up credit cards if you do not have a system in place where you track spending every month,” Kramer says. “It has to be something that appeals to you that you know you’re going to do.”

For Bell, a cash envelope tracking system helps her manage spending in different categories, including her credit card bill payment.

“When you look in a cash envelope and you see you only have $50, it’s very clear that once that money runs out there’s nothing else I can do,” she says.

4. Use credit cards for planned purchases only

Ease your way back into credit cards with small planned purchases, like a subscription service payment.

After paying off debt, Bell only uses credit cards for in-budget purchases, and she pays them off in full each month to avoid interest charges. Initially, she left her credit card at home to avoid relying on it.

5. Have an emergency fund to fall back on

An emergency fund of even $500 for a car or home repair may keep debt off of your credit cards. Start small and aim, eventually, to cast a wider safety net over time — ideally, three to six months of living expenses stowed in a high-yield savings account.

If you previously got used to budgeting a certain amount each month to pay creditors, keep that momentum going, but direct funds toward savings instead.

6. Don't store credit card info on websites or apps

Convenient payment options can sometimes lead to mindless spending. By entering payment information into forms for every online purchase, you’ll have more time to think through a purchase.

7. Get an accountability partner

A nonjudgmental partner or trusted loved one can offer input on a purchase or a stay-out-of-debt plan. An accountability partner can be a sounding board that lets you listen out loud to your own justifications for financial decisions.

8. Update your strategy

As motivations and priorities change, your stay-out-of-debt plan should follow. Continue revisiting credit card statements to identify the needs that are being met by purchases and which are most important.

If in this process you continue having frequent run-ins with debt, consider closing credit card accounts even if it can negatively impact credit scores.

“A big thing about this is knowing yourself and knowing what your challenge areas are and finding ways that work around them,” Bell says. “Five years from now it might look different, but for right now that’s what works.”